An Expensive Creditor: What Ukraine Really Gains—and Loses—Under the New IMF Programme

The Hryvnia in 2026: Will Ukraine’s National Bank Release the “Handbrake”?

06 january, 2026, 11:30

Share

One of the most fundamental questions preoccupying millions of Ukrainians—outside the context of war and peace—is the exchange rate of the hryvnia. It concerns the public even more than the notorious housing issue.

Naturally, as the country enters a new year, a significant share of Ukrainians will be interested in forecasts for the hryvnia–dollar exchange rate in 2026. But to understand exchange-rate forecasts, one must first examine the mechanisms of exchange-rate formation themselves because part of the answer is already embedded in their structure.

At present, the National Bank (NBU) is pursuing a policy of so-called exchange-rate flexibility.

Here is how this mechanism is defined by artificial intelligence:

“Exchange-rate flexibility policy in Ukraine is the National Bank of Ukraine’s strategy for a gradual transition from the fixed exchange rate of the hryvnia (introduced at the start of the full-scale invasion) to ‘managed floating,’ which allows the exchange rate to fluctuate within certain bounds in response to market conditions, while preserving financial-system stability and protecting international reserves.

The main objective is to adapt to wartime conditions, reduce imbalances in the foreign-exchange market, restore inflation targeting and prepare the ground for a return to normal monetary policy with a gradual easing of currency restrictions.”

And here is how the NBU itself defines this mechanism:

“In the early stages, the National Bank will continue to rely to a significant extent on the exchange rate as a nominal anchor for the economy. As appropriate preconditions are formed, the National Bank will gradually introduce greater exchange-rate flexibility. The gradual introduction of exchange-rate flexibility will be based on an assessment of macroeconomic and financial conditions.

As the necessary preconditions are established, the inflation target will gradually take over the role of the nominal anchor for inflation expectations, while the exchange rate will increasingly play the role of a corrective mechanism for the economy.

At subsequent stages, the National Bank will allow for greater exchange-rate flexibility, while maintaining policy consistency in order to preserve confidence in the hryvnia and in the National Bank’s actions aimed at achieving its inflation objectives.

The increase in exchange-rate flexibility will be gradual. At the initial stages, it is important to preserve maximum exchange-rate stability in order to minimize the initial shock to expectations as the National Bank moves away from its commitment to a fixed exchange rate.

To this end, the National Bank will maintain sufficiently tight monetary conditions to support the attractiveness of hryvnia-denominated assets and to avoid an uncontrolled intensification of pressure on the foreign-exchange market. In addition, the gradual easing of certain currency restrictions will help create the preconditions for a transition to greater exchange-rate flexibility.”

ВАС ЗАИНТЕРЕСУЕТ

From these two rather lengthy quotations, several conclusions become clear.

First, at the outset of the war, the NBU introduced a fixed hryvnia exchange rate, which was adjusted only a few times using administrative methods.

Second, a certain degree of macroeconomic stabilization achieved in 2023–2025 made it possible to somewhat ease currency restrictions and shift toward indirect methods of controlling the hryvnia exchange rate.

Third, a key objective was achieved: the NBU managed to prevent the emergence of so-called multiple exchange rates on the foreign-exchange market—situations in which the interbank rate differs from the official rate, while the cash market operates at yet another level altogether.

Within this model, the NBU ostensibly no longer sets the exchange rate administratively, as it did at the start of the war. Instead, the rate is “set” by the interbank foreign-exchange market. At the same time, the interbank market itself is largely controlled by the National Bank through currency interventions. Thus, the NBU no longer “controls” the hryvnia exchange rate directly; rather, it controls the interbank market, which in turn establishes the rate. This is a kind of “derivative” regulation system.

But what kind of “restoration” of inflation targeting is the NBU talking about?

The point is that monetary economics recognizes a concept known as the “impossible trinity”—the idea that it is impossible to simultaneously achieve three objectives:

- a fixed exchange rate;

- free movement of capital;

- independent monetary policy (inflation control through interest-rate policy).

Only two of these options can be chosen at the same time.

At the start of the war, the NBU blocked capital flows (2) and fixed the hryvnia exchange rate (1). This left no room for inflation targeting (3). That is why, in the first months of the war, the NBU “froze” the policy rate at 10 percent. The result was a stable exchange rate, but inflation spiraled out of control, reaching 26.6 percent by the end of 2022.

In the second half of 2022, the NBU raised the policy rate to 25 percent, thereby restoring inflation targeting (3). At the same time, the regulator never fully chose a second option, instead “nibbling at” the other two simultaneously: maintaining a quasi-fixed exchange rate (1) and a quasi-free movement of capital (2).

With some caveats, one could even say that the NBU decided—perhaps for the first time in the history of monetary economics—to attempt the impossible: to pursue all three objectives of the “impossible trinity” at once.

To some extent, this would of course be an exaggeration, since the National Bank has merely been “taking small bites” of all three apples of monetary policy. The exchange rate appears to be controlled, yet there is both an interbank and a cash market, and the rate does fluctuate—albeit within a narrow corridor.

Capital movement is ostensibly blocked, but certain loopholes exist—for example schemes involving the outflow of foreign currency abroad under fictitious imports.

This simultaneous focus on all three options has led to a situation in which, aside from exchange-rate stability (achieved largely thanks to external assistance), the NBU has failed to formulate an independent monetary policy—i.e., to bring inflation under control without destroying the objectives of economic growth.

That is precisely why inflation in Ukraine remains significantly above the NBU’s target: the target is 5 percent per year, while actual consumer inflation reached 10 percent by the end of 2025.

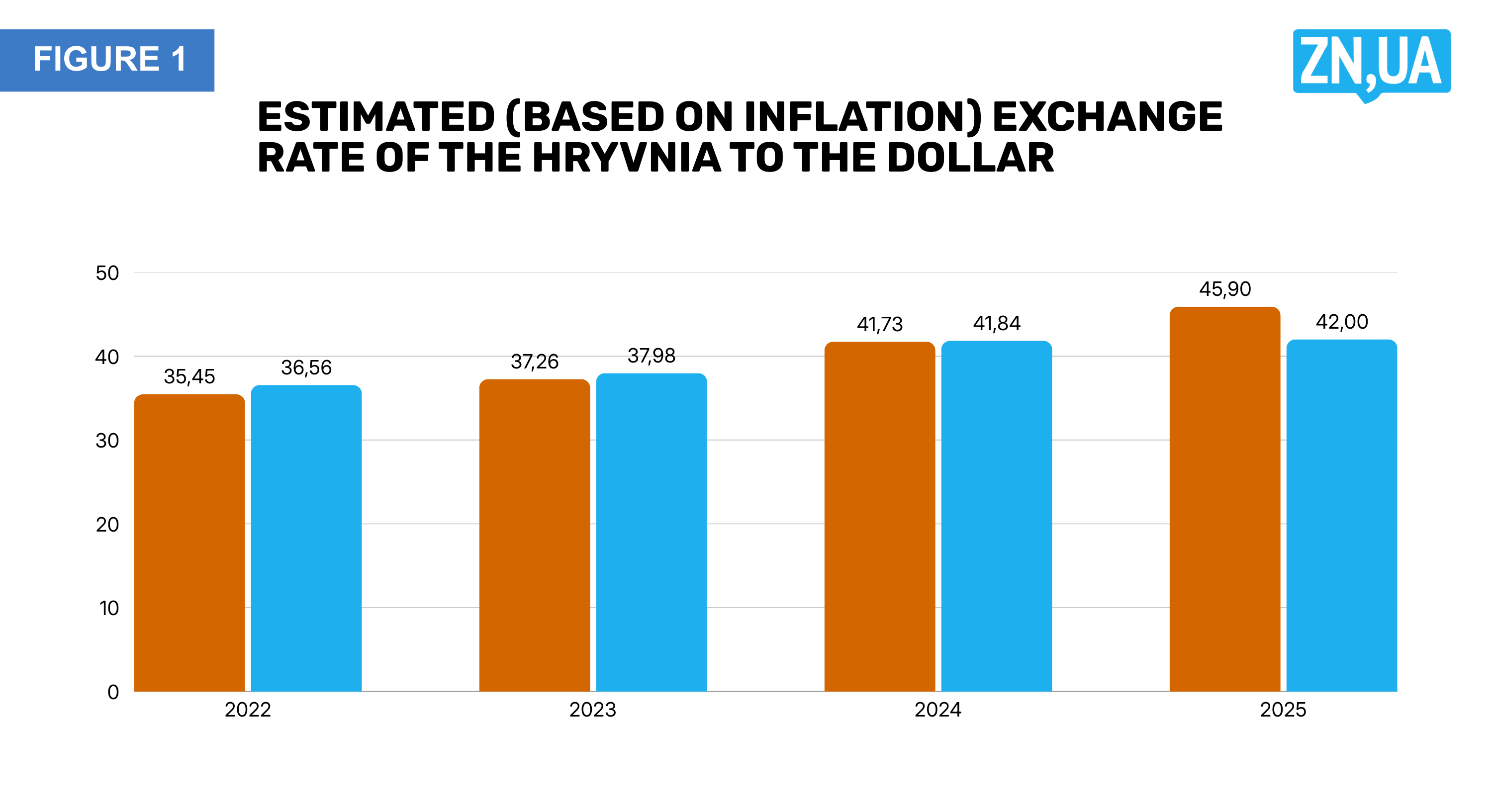

Figure 1 shows the calculated hryvnia–dollar exchange rate (based on hryvnia inflation) and the actual rate. As can be seen, in 2022–2024 the actual exchange rate almost fully corresponded to the calculated one. In other words, the NBU acted quite simply: it took the hryvnia–dollar exchange rate at the beginning of the year and adjusted it over the reporting period by the inflation index. As a result, the actual exchange rate at year-end almost entirely coincided with the calculated rate (adjusted/indexed to inflation).

ZN.UA

Knowing this small “secret,” one can “guess” the hryvnia exchange rate based on planned inflation indicators. For example, if inflation in 2026 amounts to 10 percent, the hryvnia would also depreciate by 10 percent. However, in 2025 this model broke down for the first time since the war began: the calculated exchange rate should have been close to 46, while the actual rate remains around 42.

ВАС ЗАИНТЕРЕСУЕТ

This has led to rising domestic prices in dollar terms and to a growing attractiveness of the domestic market for imported goods. At the same time, domestic producers saw a sharp erosion of price competitiveness. This also negatively affected exports: exporters lost part of their foreign-currency revenues in hryvnia terms. In turn, the state budget missed out on substantial funds: a significant share of tax revenues in Ukraine comes from VAT on imported goods, and this indicator typically increases during hryvnia depreciation. Consequently, the state lost tens of billions of hryvnias in tax receipts.

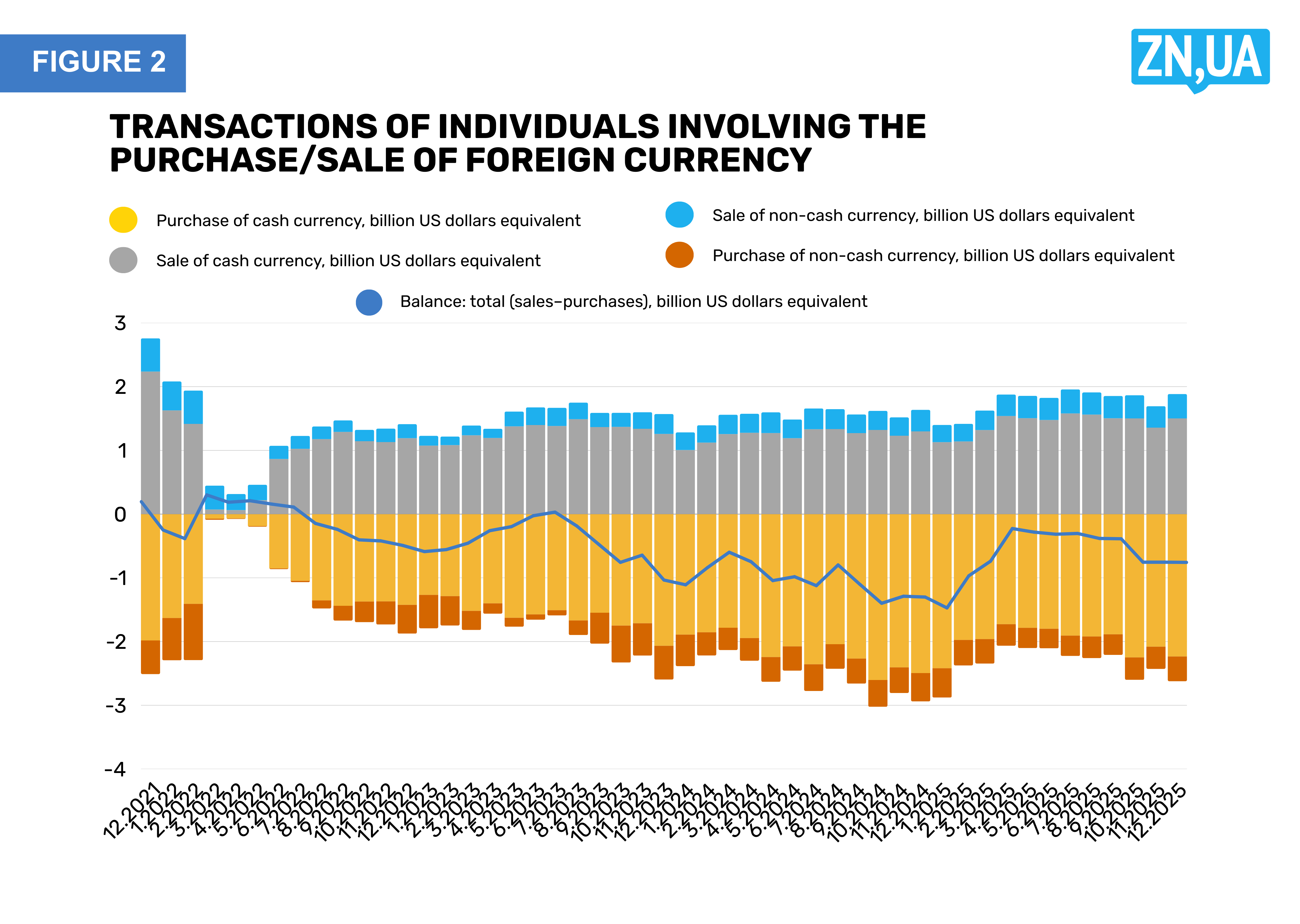

Incidentally, Ukraine’s negative trade balance (goods and services) in 2025 stands at minus $53 billion, or 25 percent of GDP. This is an enormous deficit, which for now is balanced only by external support and is, in essence, a very dangerous “compressed spring.” It should therefore be gradually “released” by depreciating the hryvnia exchange rate (see Figure 2).

ZN.UA

This raises a logical question: if a “slight” depreciation of the hryvnia is so beneficial to everyone, why does the NBU not do it? In reality, there are several answers—and all of them are valid.

First, the NBU’s key objective is inflation control. Only a handful of meticulous experts will question the central bank about economic growth; everyone else will question it about inflation.

Given Ukraine’s enormous dependence on imported goods at present, a 10 percent depreciation of the hryvnia would become a significant pro-inflationary factor. According to forecasts, inflation in 2025 will amount to 9.2–10 percent, which is well above the 5 percent target. A 10 percent depreciation of the hryvnia in 2025 would therefore add up to 2 additional percentage points to inflation, pushing it to around 12 percent—into double-digit territory. The NBU is now highly focused on bringing official inflation back into single digits—at least to 9.99 percent.

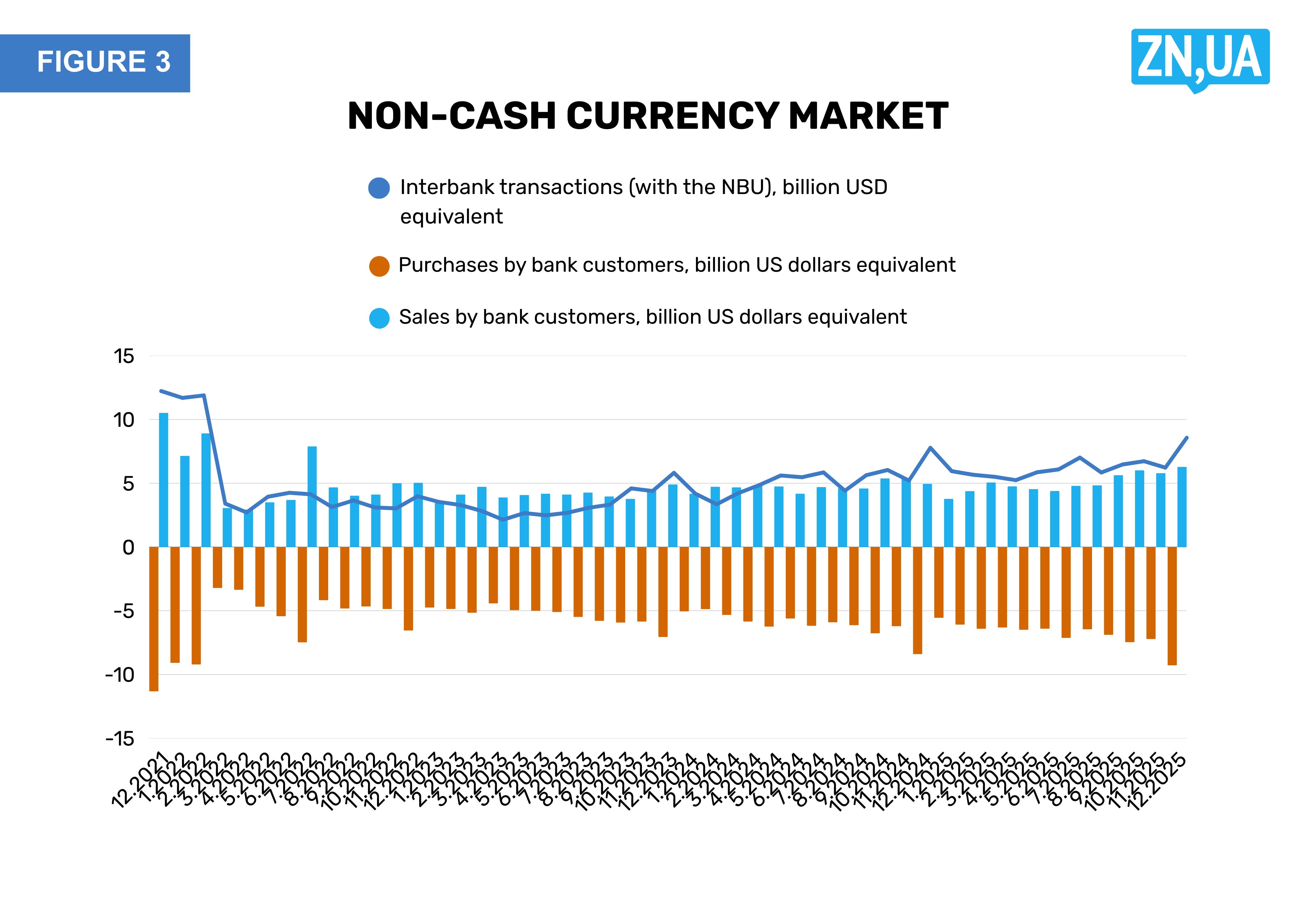

Second, the NBU has created a kind of “feeding trough” for banks (see Figure 3) in the form of the deposit certificates scheme, which has already absorbed more than UAH 200 billion in public funds (an unofficial subsidy from the NBU to a group of commercial banks).

ZN.UA

A depreciation of the hryvnia could slow the inflow of hryvnia funds from households into banks and even trigger a certain reversal of deposits—“flipping” hryvnia deposits into foreign currency. As a result, the scale of this “feeding trough” would shrink.

That said, there are also objective factors: a sufficiently large depreciation could necessitate a new cycle of policy-rate hikes, which would provoke criticism from the productive sector of the economy.

In addition, part of imports consists of armaments and components for the defense-industrial complex, as well as fuel. Price increases in these categories during wartime are undesirable.

ВАС ЗАИНТЕРЕСУЕТ

Ukraine’s current economic situation is such that a hryvnia depreciation would be a very weak stimulus for exporters (against the backdrop of destroyed grain and oilseed terminals at ports and persistent logistics problems). At the same time, depreciation would simply make imports more expensive.

On the other hand, why further undermine exporters with a “stable” hryvnia exchange rate? For the procurement of components for the defense-industrial complex, a “special exchange rate” could be used. But this immediately raises another dilemma: corruption—because a whole “pack of Mindich-like people” would instantly rush in and stock up on foreign currency at a favorable rate, ostensibly for imports for defense needs.

There is yet another factor. The fact that the NBU is simultaneously “biting into” all three apples of monetary policy deprives it of the ability to effectively target inflation.

The National Bank has opted for inflation targeting combined with a seemingly flexible, quasi-market exchange rate, while simultaneously shaping a trend toward the gradual removal of administrative barriers to capital outflows from the country. There is a powerful demand for this among political elites: profits during the war do exist, but straightforward channels for taking capital out of the country do not.

Accordingly, any IMF demands for a “manual devaluation” are, for the time being, rejected by the NBU on the grounds that the “impossible trinity” does not allow it—and that such steps could call into question the policy of easing currency restrictions (which business is said to be eagerly awaiting).

At the same time, the most appropriate model under current conditions would be an exchange-rate corridor, or a so-called “currency snake.” This model was successfully used in Europe to help countries with weak national currencies adapt to European integration standards.

Accordingly, for 2026 the corridor declared by the NBU should be set at UAH 45 per dollar, with a ±5 percent band for depreciation or appreciation—that is, a range of UAH 42.75–47.25 per US dollar.

However, such a move could undermine the deposit-certificate schemes, as it would reduce the inflow of hryvnia resources into banks. These funds do not enter the real economy in the form of lending in any case; they perform only an immobilizing, sterilizing function within the disinflation program. And even then, as we can see, not entirely successfully: inflation remains high, while bank profits and returns on equity are at historic highs. Moreover, steering the exchange rate into a corridor would slow the liberalization of capital outflows from the country. And there are plenty of actors eager to take their “profits” out of Ukraine through legal channels rather than via cryptocurrency on flash drives. And this is where things stand.

Noticed an error?

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Stay up to date with the latest developments!

Subscribe to our channel in Telegram

Пожалуйста выберите один или несколько пунктов (до 3 шт.) которые по Вашему мнению определяет этот комментарий.

Пожалуйста выберите один или больше пунктов

Нецензурная лексика, ругань

Флуд

Нарушение действующего законодательства Украины

Оскорбление участников дискуссии

Реклама

Разжигание розни

Признаки троллинга и провокации

Другая причина

Отмена

Отправить жалобу

ОК

Login with Google

Login with Google