Debt Repayment: What Ukraine Offered to Its Creditors and What Response It Heard

Ukraine wants to restructure a fifth of its foreign debts. Why and under what conditions — let's figure it out.

The claim that Ukraine is not fighting a war in the country for its own money is a hostile and frankly false narrative. For the most part, monetary aid from allies is provided to us in the form of loans, but the share of grant (i.e., non-refundable) support, on the contrary, is decreasing — from 29% in 2023 to 12% in 2024. So, at the moment, we have to return almost all the funds we receive. At the same time, another common statement about "debts that will be paid off by our grandchildren" is also false. The terms of repayment of our debts are much shorter, which makes the issue of our national debt so acute.

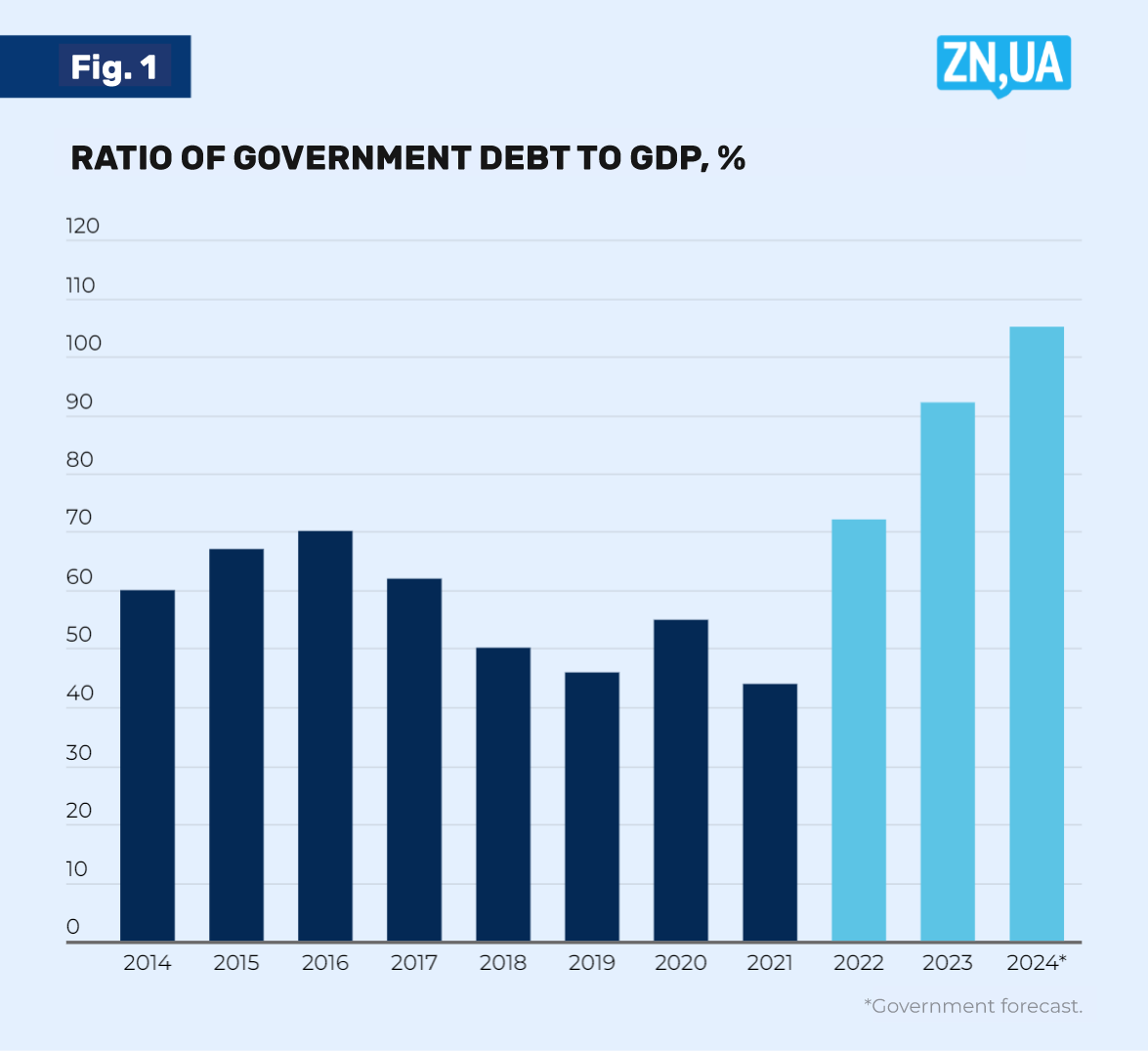

To assess how waging a full-scale war with Russia has affected our debt sustainability, let's look at the ratio of our national debt to our own Gross Domestic Product (GDP): at the end of 2021, it was a rather modest and relatively safe for financial sustainability 43.3%, at the end of 2024, according to government predictions, it will already be 104.6% of Gross Domestic Product (GDP) (see Fig. 1). Immodest and dangerous debt, considering that our economy is not in the best shape.

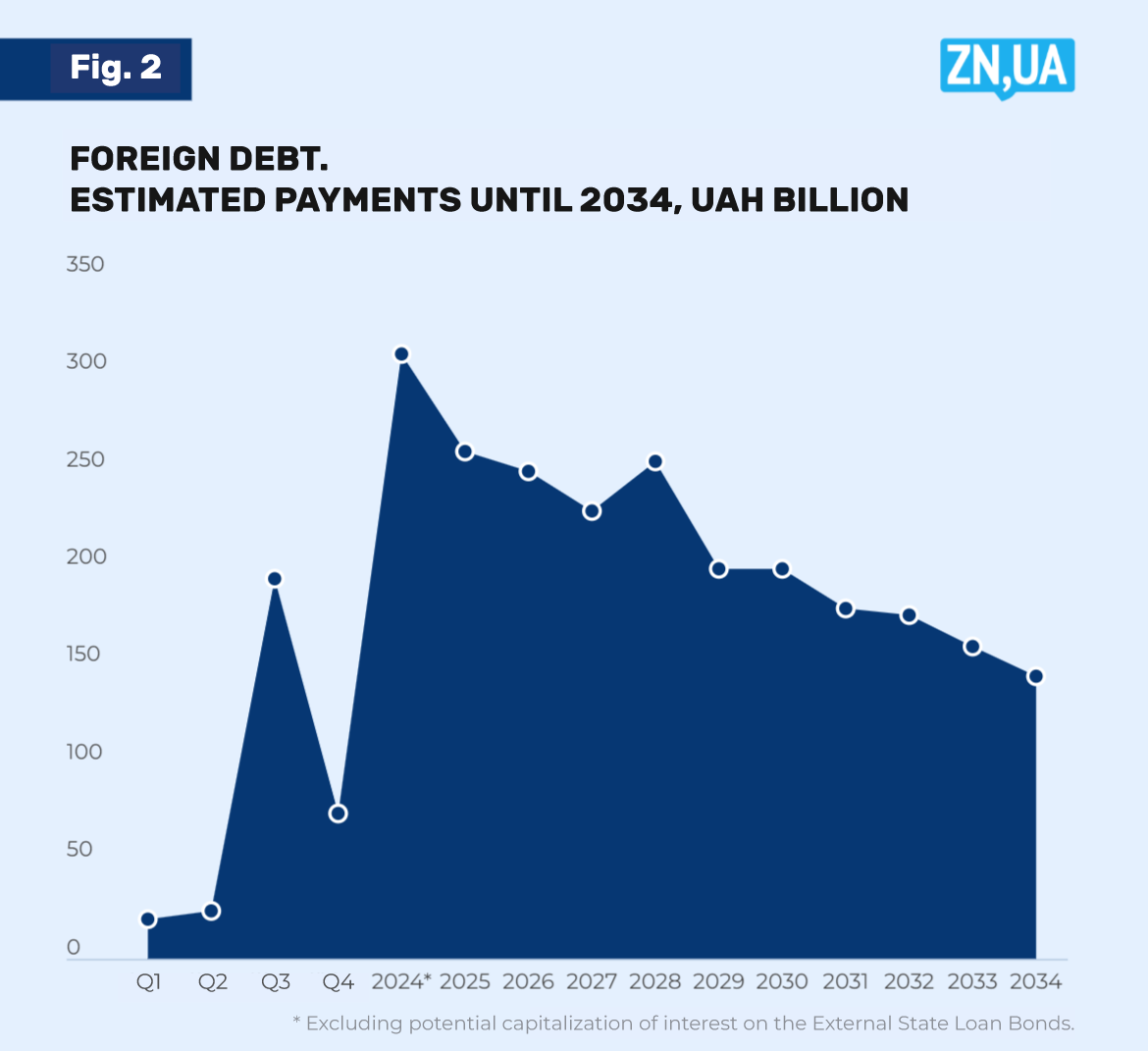

To assess the speed of the approaching crisis, it is worth looking at our projected payments on foreign loans: the first quarter of 2024 —19.8 billion UAH, the second quarter of 2024 — 23.05 billion UAH, the third quarter of 2024 — immediately almost 195 billion UAH. Yes, later in the fourth quarter, there will be a "slight" decrease to UAH 75 billion, but this will be only a short pause to take a breath before the multi-year marathon of foreign debt repayment (see Fig. 2).

The surge in the third quarter marks the end of a two-year moratorium on the return of debts for 24 billion dollars in Eurobonds. Holders of 4 of these 24 billion dollars are creditor countries (Canada, France, Germany, Japan, Great Britain, and the USA), which have already confirmed that they are ready to extend the moratorium until the end of the current program of the International Monetary Fund (IMF), that is, until 2027. The remaining 20 billion dollars belong to private borrowers, with whom it is not so easy to negotiate, especially since we continue to properly service the rest of the old debts all this time (except for the legendary "three billion of Yanukovych"), and this leaves the creditors "under moratorium" with an unpleasant impression. Since they don't want to extend the moratorium, and we definitely won't be able to return everything at once, the parties had to start difficult negotiations.

This process is not easy because some creditors are not what they need to be, conversations about restructuring in principle cannot be simple, the final solutions rarely satisfy both parties, and most importantly, in the process, instead of simplifying, we still manage to complicate our lives — proven by the Gross Domestic Product (GDP) warrants from the former Minister of Finance of Ukraine Natalia Yaresko. Actually, this "warrant" experience is the reason why the current restructuring needs careful evaluations, and we thank the London Stock Exchange for the publicity of these negotiations.

Proposals of the parties

In fact, negotiations are ordinary market bargaining, only in expensive suits and with the participation of financial consultants. But it is too primitive and simple to ask for the maximum in order to get something average, it never works out because all the participants calculate too well. Therefore, usually something simple and familiar like 60% was written off is not born in the process. Even if you see such a headline, it is almost certain that this was not the case and there was something else important in this process, and the final conditions and terms may be such that simply writing off some interest will no longer seem like a success.

Actually, that is why the best strategy for us would be to at least conduct negotiations on extending the moratorium until 2027, and at the most it would be good to conduct negotiations on writing off this debt as such. Unfortunately, the "maximum" option was not even considered, and the "minimum" option, although there was one, did not make it to the public announcement. So, we started inventing some completely new and non-standard way out of the current situation.

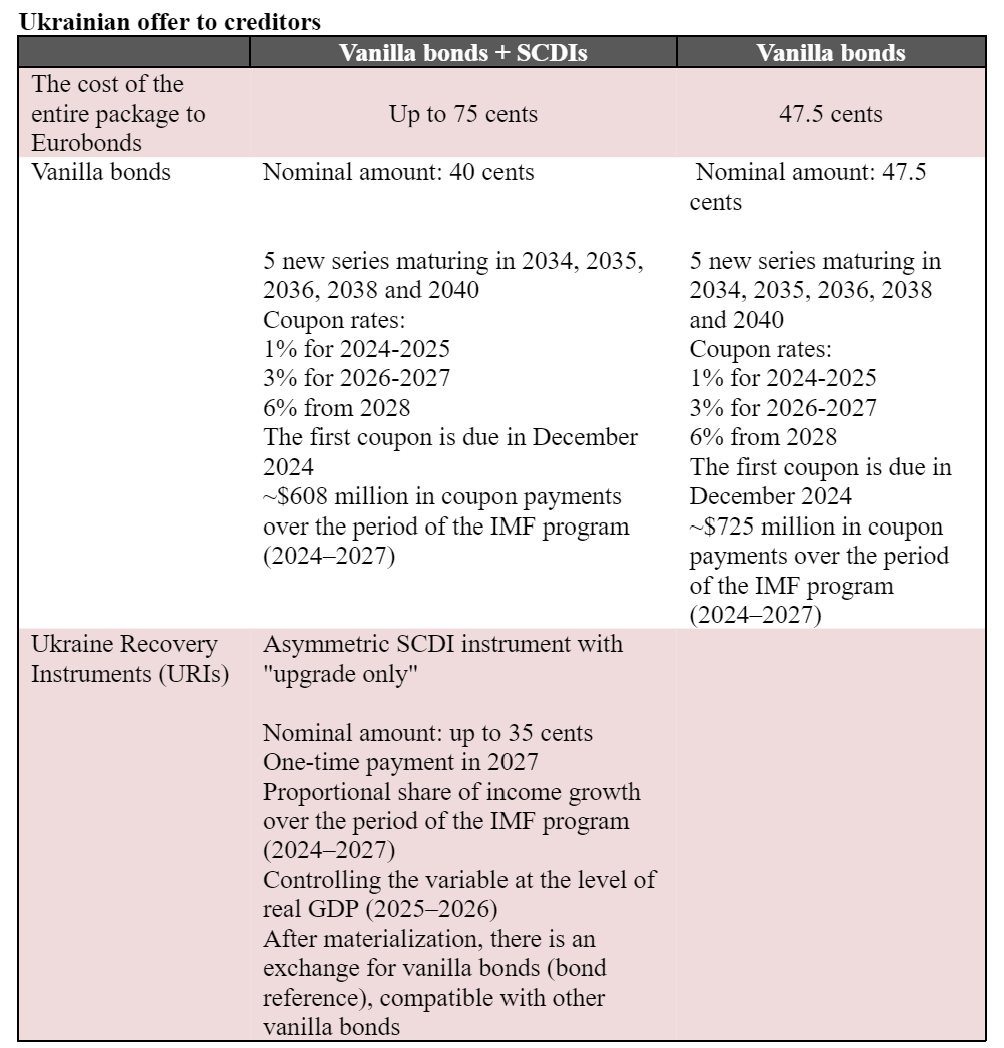

Creditors are offered two options (check the table to make sure we're not looking for an easy way out of this situation again).

To put it simply, creditors were offered to exchange their (more precisely, our) Eurobonds for a package of vanilla bonds (that is, basic bonds, like vanilla ice cream in a cup) with fixed income and a symbolic coupon payment, and if desired, use an additional debt instrument (URIs) that is connected to our economic growth.

In particular, by choosing the first option, the owners will receive vanilla bonds at the rate of 400 dollars for every 1,000 of the principal amount of the bonds and interest (with single repayment terms in 2034, 2035, 2036, 2038 and 2040). In addition to all this, they will receive an additional URIs tool — 350 dollars for every 1,000 dollars principal amount of Eurobonds exchanged. There will be no payments for URIs, this instrument gives the owner the right to receive vanilla bonds in 2027, provided that Ukraine reaches the indicators of the International Monetary Fund (IMF) base scenario in terms of income and Gross Domestic Product (GDP), i.e. shows an average annual growth rate of the economy of at least 5%.

This option looks more profitable than the alternative, namely to take vanilla bonds without URIs at the rate of 475 dollars per thousand. However, only under the condition that our economy will grow confidently in the coming years and the Gross Domestic Product (GDP) will exceed UAH 10 trillion in 2027. If not, then choosing plain vanilla bonds at 475 is not such a bad decision.

At least this is how the Ukrainian side sees this whole story, expecting to write off, if not 60% of the debt, then at least a quarter.

Instead, the creditors offered the Ukrainian side a slightly different option, namely a set of two instruments. The first of them is actually our vanilla bonds, simple bonds that will exchange 40% of the principal amount of the debt for Eurobonds and interest. The only difference is that the rate for them will be 7.75% immediately, with payments in 2034 and 2035... The second instrument — Recovery Bond — is more complicated, with a variable coupon, although also with a write-off of 62.5 %, but the rest of the conditions are tied to the compliance of our economic results with the predictions of the International Monetary Fund (IMF) and, as in the case of Yaresko's Gross Domestic Product (GDP) warrants, God forbid economic growth will still happen.

In general, the desire to get the most out of the Ukrainian economy, which is barely starting to recover, is not inspiring. Especially considering that our offer is already quite generous.

So, as we can see, creditors are psychologically ready to write off 60% of our principal debt. But not out of love for us and not because our country is so good at negotiations and has achieved some exceptional treatment. Objectively, no one gives more than 30% of the nominal value for our Eurobonds for a long time, and there is frankly no demand for them. The very possibility of selling them (which, in fact, involves exchanging them for new papers), and not for 30%, but for 40%, is a gift for our creditors.

We can debate whether we should give this gift, because technically we have been in default for a long time and we have more than reasonable grounds for it.

Preserving the reputation of a responsible borrower for the sake of being able to return to the foreign market of private loans is a good excuse for this return to be real for us at least in this decade.

However, we still have to try to solve the situation we have now, especially since negotiations are in progress and our side still has a chance to reach a more or less acceptable, that is, the least burdensome and most suitable for the country, result.

The best design in this case should be as concise as possible, without additional variables tied to economic indicators and any predictions. We do not know what Ukraine will be like in 2034, when it will return coupon payments to creditors. No one, including the International Monetary Fund (IMF), knows this.

***

Thus, since the beginning of the full-scale invasion, we have been attracting mainly concessional external loans, that is, from the start, they provide for better than market conditions, both in terms of interest and terms. Usually, our new loans involve deferring payments for ten years. But there are still domestic debts, which currently amount to UAH 1.6 trillion, and they will definitely grow, there are "old" (deferred and not very deferred) debts, there are debts guaranteed by the state. And the current terms of postponement will pass quickly. Ten years is actually not a very long time. Look around — three of them are almost gone.

At the same time, the restructuring of the fifth part of our debt, whatever it may be, does not remove global issues: what to do with other loans, how to get out of a situation when the country's debt is greater than its Gross Domestic Product (GDP), how to distribute payments over time in such a way as to avoid peak loads, and in general, how to plan at least something for the future of at least ten years?

Our current public debt management strategy expires in 2026…

Read this article in Ukrainian and russian.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google