Rapid Post-War Recovery: Is It Possible in Ukraine?

An 800 Billion Plan: What Can Be Offered to Investors Besides Made in Ukraine Label?

16 january, 2026, 11:45

Share

Next week, on the sidelines of the economic forum in Davos, Ukraine plans to sign an Economic Prosperity Plan with the United States, the European Union and the G7. The announced figure of $800 billion, voiced by President Volodymyr Zelenskyy, fully matches the grandiosity of the document’s title. The amount is expected to consist of private investment, grants, loans and equity capital. However, if you let yourself get carried away by visions of genuine prosperity, a new comprehensive development plan and hundreds of billions of dollars in investment—don’t. Although the plan publicly envisages the participation of the EU and G7 partners, there are strong suspicions that it was prepared purely “for display,” with the number of zeros intended to impress one single person in the Oval Office.

ZN.UA’s government sources are convinced that we will see nothing fundamentally new in the finalized documents—neither in the framework agreement nor in the roadmap accompanying the plan.

First, government officials simply did not have time to develop a substantively new strategy with unconventional approaches and economic creativity. Or rather, time was abundant: back in April 2022, ZN.UA wrote that it was precisely the moment to begin designing a new Ukraine and a modern economy, so that after the war the country would not be forced, out of desperation, to rebuild the remnants of the Soviet legacy. But who in government read that—let alone acted on it? As a result, the task of conjuring up hundreds of billions of dollars’ worth of investment projects—within a framework of multi-track cooperation—landed on government officials out of the blue.

Second, the core of the negotiating team on economic cooperation—Prime Minister Yuliia Svyrydenko and Economy Minister Oleksii Sobolev—are people who over recent years have been engaged almost exclusively in producing plans and strategies of various kinds. Time and again, these documents have recycled a mix of unoriginal “new” ideas and long-forgotten old ones—a habit we have repeatedly called them out on. Expecting an intellectual breakthrough after years of uninspired paperwork would be naïve. Back in the spring of 2022, we argued that the authorities should bring in external experts—above all futurists and economists—to think about Ukraine’s long-term future while the government was busy “putting out fires.” But once again, no one in power was listening. As a result, we are likely to see yet another collage of Ukraine’s familiar proposals in energy, infrastructure and processing.

Third—and most importantly—our economy is currently nowhere near ready to absorb such volumes of investment, even if they were to materialize.

Absorptive capacity

No matter how much money is poured into an economy, its ability to absorb it is limited by the size of that economy and its level of development. There are numerous constraining factors, ranging from the availability of labor and the technological structure to the textbook issue of demand for produced goods. Even our current primitive economic model, whose entire foundation rests on the cultivation and export of grain, faces a purely physical constraint: the area of arable land.

Somewhere back in the early 2000s, when industrial products and agricultural raw materials accounted for 70 and 30 percent of our exports respectively, we might still have dreamed of an investment boom. Today, however, things have taken a U-turn: industrial goods make up a mere one-fourth of exports, while agricultural raw materials command as much as 75 percent. Oleksii Kushch has explained in detail why, in conditions of deindustrialization and an “industrial desert,” even military production is not a viable scenario for Ukraine. We will instead focus on the ability of the current Ukrainian economy to “digest” $800 billion, even if spread over ten years.

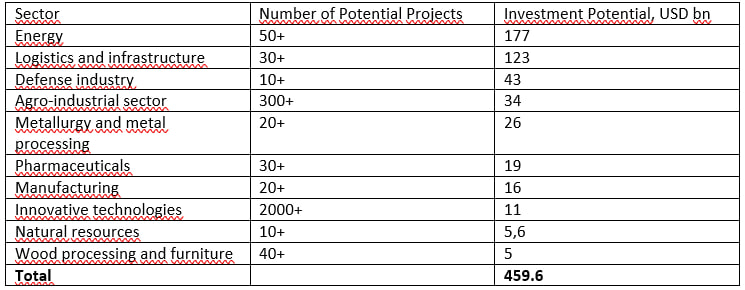

At the end of 2022, the answer to this question was provided by Ukraine’s Ministry of Economy itself in the course of preparing the government’s Advantage Ukraine investment initiative. At the end of 2022, Ukraine’s investment potential was estimated at $460 billion (see Table 1), with a footnote acknowledging that full realization of this potential was impossible, yet the figure was still presented to investors as an upper bound.

Table 1. Ukraine’s Investment Potential

#AdvantageUkraine

After criticism of the unrealistic nature of these proposals—based on the argument that investors need specific projects with clear potential, not abstract potential without substance—the Ministry of Economy “slightly” revised Ukraine’s investment capacity. In 2025, it released a catalogue of 250 concrete investment projects with a total value of $40 billion (see Table 2).

Table 2. Investment Project Portfolio

|

Sector |

Number of projects |

Required financing, USD bn |

Project categories |

|

Energy |

75 |

26.9 |

Renewable energy sources; biofuels and biomethane; balanced energy supply systems; nuclear energy; cogeneration; electricity distribution and transmission; oil and gas; hydrogen |

|

Industry |

39 |

1.2 |

Automotive and public transport; rail equipment; engines and turbines; pipe production; electronics and optics; specialized equipment; chemical industry; packaging; textiles; wood products; paper products |

|

Agro-industrial complex |

30 |

1.4 |

Crop production; livestock; dairy farming; infrastructure; deep processing; oilseed processing; chemical industry |

|

Transport / logistics |

18 |

1.6 |

Railway infrastructure; maritime infrastructure; export logistics; rolling stock and river fleet renewal; intermodal transport; warehouse infrastructure development |

|

Digital technologies |

18 |

0.8 |

IT infrastructure projects; digitalization of the economy; innovation development; products and services |

|

Healthcare |

16 |

0.5 |

Pharmaceutical manufacturing; nuclear medicine; pharmaceutical supply chains; new healthcare facilities |

|

Defense |

13 |

0.2 |

UAVs; communications systems; AI-based software; drone detection systems; unmanned ground vehicles; counter-drone systems; demining systems |

|

Critical materials |

12 |

2.4 |

Graphite; titanium; beryllium; lithium; uranium; polymetals |

|

Construction materials and structures |

11 |

0.5 |

Building materials and structures; float glass plants; insulation materials |

|

Real estate and housing |

9 |

0.4 |

PropTech; commercial real estate; retail property and leasing; cultural heritage; industrial parks |

|

“Green” steel |

3 |

2.1 |

Low-emission steel; DR-grade pellets; tailings thickeners |

|

Private capital and investment funds |

6 |

2.0 |

Funds focused on high-impact sectors (technology, logistics, agro-industry, manufacturing, real estate, energy), post-war reconstruction, and innovative enterprises |

|

Total |

250 |

40 |

Source: #AdvantageUkraine

To avoid the impression that we are deliberately ignoring the fact that the Prosperity Plan speaks of $80 billion per year, we suggest taking a closer look at the $40 billion project categories. Many of these projects are designed for multi-year implementation, which in no way altered the final—and far more modest—total figure.

But surely new projects can be invented?

They already exist.

Prime Minister Yuliia Svyrydenko has enough of this paperwork for three prime ministerial terms. Why not pull a few more items from the government’s public investment portfolio? Its total value stands at $250 billion. True, about one-third of it consists of “mothballed” projects from the 2010s, whose implementation should, at the very least, undergo an additional feasibility test today. There is reason to suspect that the country’s current priorities have drifted somewhat away from building a new pretrial detention center in the village of Martusivka or modernizing a water pipeline in Chernivtsi.

Organizational incapacity

What this boils down to is simple: in theory, we could absorb up to $400 billion; in practice, no more than $40 billion; yet after a bit of tidying up and donning white trousers, we are supposedly ready to take a swing at $800 billion.

We will dazzle investors with our promises; they will put in their hard-earned money—and even shake Russia down for reparations, all for the sake of our prosperity.

We would not say this is impossible—but it is highly unlikely. The story of already frozen Russian assets makes it abundantly clear how illusory the prospects of future reparations actually are. And to genuinely interest investors, Ukraine must undertake an enormous volume of preparatory work.

This is easiest to illustrate using the defense-industrial complex. In the prospective plan, its investment potential is listed at $43 billion; in the investment project portfolio, it amounts to a pitiful $0.2 billion, spread thinly across 13 projects. And yet, in 2025, $1.8 billion was invested in Ukraine’s defense industry for weapons production under the “Danish model”. In addition, Ukraine submitted its own defense-industrial projects under the SAFE mechanism, which integrates Ukraine into the European defense ecosystem, with expected financing of $5 billion. Together, this amounts to almost $7 billion in investment—not the theoretical $43 billion, but far more than the government’s planned $0.2 billion. This investment breakthrough, however, would have been impossible without joint infrastructure created with European partners—or, more accurately, with their assistance—including special financial and investment mechanisms.

Thus, to implement the Prosperity Plan, Ukraine would require a fundamentally different economy—not even the economy of 2021.

Nor will the participation of the EU and the G7 in the process serve as a guarantee of success. It is true that cooperation with European partners in the defense sector has produced tangible results, and their motivation to develop armaments is understandable. However, the search for new investment mechanisms in other, less attractive or more competitive sectors, is unlikely to be equally swift or transformative—especially given that the most attractive asset of all, mineral resources, has already been chartered by the US–Ukraine Investment Fund.

By the way, let us recall this much-touted breakthrough. Everything is proceeding strictly according to plan: from its official launch on 23 May 2025, it took the Fund seven months to launch a website for accepting applications and to announce, in early 2026, its readiness to attract investment.

A tangible achievement could have been the approval of investors for the Dobra Site lithium deposit. Yet despite the fact that by all metrics this project is a jewel in the portfolio of any fund, none of the official communications surrounding it made any reference whatsoever to the American–Ukrainian Fund. The tender was conducted and completed “outside the Fund” and prior to the launch of its official website. Unpleasant thoughts even emerged that the Fund itself might not, in fact, be particularly necessary for attracting investment into subsoil development.

The auction for developing the Dobra deposit was won by a duo of globally recognized companies—TechMet and The Rock Holdings. To put the numbers in context: the deposit was valued at $179 million in capital investment, of which $12 million will be allocated to geological exploration and an international audit of reserves, and $167 million to organizing extraction, should the reserves be confirmed. This is Ukraine’s best-prepared and most advanced site.

To understand the state’s gains: under the contract terms, Ukraine’s share of profitable output will range between 4–6 percent. As for other gains and advantages, one should ask the Dobrovelychkivka community, on whose territory the Dobra site is located—and which the central authorities systematically excluded from all stages of preparing the terms of the 50-year contract with the investor.

ВАС ЗАИНТЕРЕСУЕТ

In other words, one should not be enchanted either by the figures of yet another plan or by the prospects of its implementation—especially at the local level.

Nor should we forget about risk as a determining factor for any investment.

No matter how attractive Ukraine’s proposals may be, an investor will not even approach them without analyzing potential losses—military, as demonstrated by the strike on a coffee-machine manufacturer in Mukachevo, where neither American investment nor the presumed safety of the location provided any guarantees; and political, recalling how swiftly BlackRock signed a broadly worded memorandum with Ukraine, heavy on good intentions, only to curtail all activity just as rapidly due to “uncertainty” following Donald Trump’s election as US president. Against this backdrop, it is altogether strange that we have already begun talking about investment and prosperity without any understanding of how to reduce the risks investors currently face.

Even stranger is the rush to sign something without thoroughly thinking through what exactly we need, what kind of economy we intend to develop, which specific projects we will pursue and in what stages they will be implemented. Do we have the necessary financial instruments? Is the level of currency liberalization sufficient? Do we have free capital movement, insurance products, an adequate labor force, demand and access to markets? Ten years might barely suffice just to prepare all of this.

ВАС ЗАИНТЕРЕСУЕТ

But so be it—if something needs to be signed, we will sign it. We already have so many plans, programs and funds; one more will not make a difference. We are still waiting for quantity to finally turn into quality.

Ultimately, this may become a highly instructive case demonstrating that reforming—and indeed modernizing—the state and its economy is necessary not because the IMF might withhold a loan or the European Commission might point to “limited progress,” but because a genuinely interested investor may appear—and you will have nothing to offer them except a Made in Ukraine label and an empty hangar in an industrial park.

Noticed an error?

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Stay up to date with the latest developments!

Subscribe to our channel in Telegram

Пожалуйста выберите один или несколько пунктов (до 3 шт.) которые по Вашему мнению определяет этот комментарий.

Пожалуйста выберите один или больше пунктов

Нецензурная лексика, ругань

Флуд

Нарушение действующего законодательства Украины

Оскорбление участников дискуссии

Реклама

Разжигание розни

Признаки троллинга и провокации

Другая причина

Отмена

Отправить жалобу

ОК

Login with Google

Login with Google