Will Ukraine Have Enough Gas For Winter? Time To Move From Emergency Purchases To Strategic Partnerships

Ukraine's energy security will remain one of the key challenges for the state in the coming years, even if active hostilities come to an end. Post-war recovery will require additional electricity and gas. Against this backdrop, Ukraine must seriously revise its gas strategy, relying not only on increasing its own output but also on integration with the European market and long-term contracts for LNG supplies, primarily from the US.

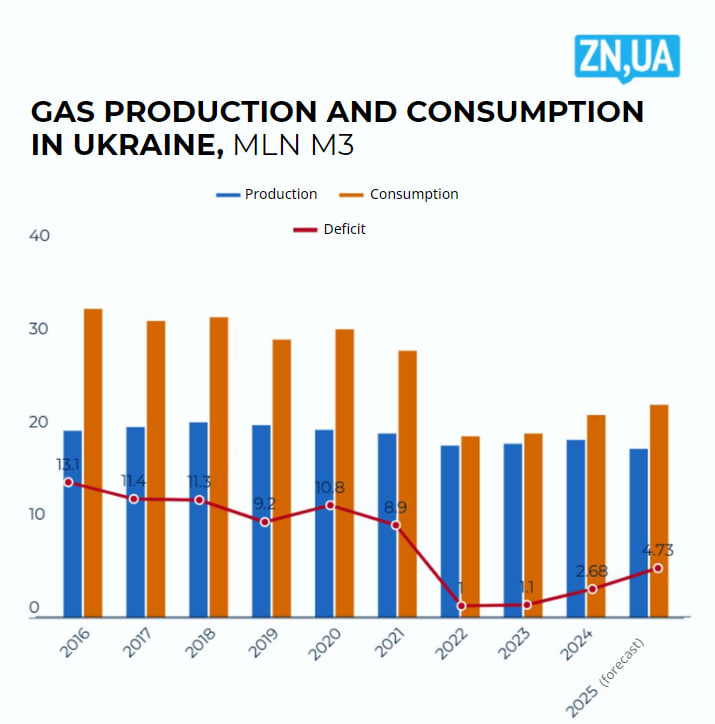

Why Ukraine needs gas imports

According to estimates by Naftogaz of Ukraine, Ukraine will need to import 4.6 billion cubic meters of natural gas for the next heating season. Independent experts rate the import needs at 5.5–6.3 billion cubic meters of gas. This amount is only partly due to Russian attacks on Ukrainian production. The main reason is the gradual recovery of the economy and growth in gas consumption. In 2024, according to my estimates, consumption will increase by 10 percent to 21.80 billion cubic meters, but domestic production will grow by only 2.2 percent to 19.12 billion cubic meters, which is even less than pre-war production in 2021 (19.8 billion). After the strikes on production facilities, output in 2025 could fall to 18.16 billion cubic meters, while consumption will increase to 22.89 billion, creating a gas balance gap of 4.73 billion cubic meters that will have to be imported (see figure).

Unfortunately, despite all the bold statements by politicians that Ukraine will soon become self-sufficient and abandon gas imports, no significant growth in production has been observed. This is mainly due to the depletion of Ukrainian gas fields and the lack of new large deposits. I personally believe that Ukraine's only chance to ramp up production significantly is to develop gas output on the Black Sea shelf. However, this requires not only the end of the war and billions in investments but also 5–10 years of active work. Therefore, Ukraine will have to import 4–6 billion cubic meters of gas annually for a long time to come.

Nonetheless, there is nothing new or critical about gas imports. Ukraine imports almost all of its gasoline and diesel fuel. Many countries import gas, and their economies are actively developing notwithstanding. For example, Poland imports 70–75 percent of its gas consumption, with LNG accounting for 50 percent of imports. Since gaining independence, Ukraine has always consumed more gas than it produced, importing the difference. Until 2015, our country imported gas from Russia, and after that, only from European gas markets. Currently, Ukraine mainly buys gas on spot markets rather than under long-term contracts. This creates significant risks and fluctuations in purchase prices.

Therefore, given Ukraine's long-term need to import 4–6 billion cubic meters annually, the state-owned Naftogaz company should consider the possibility of independently entering the LNG market and purchasing liquefied gas directly from American, Qatari and other producers. At the same time, Ukraine could receive at least 2 billion cubic meters of gas per year under long-term contracts. LNG could be supplied to Ukraine through the developed LNG infrastructure of Poland, the Baltic countries and Greece (via the Trans-Balkan pipeline).

Naftogaz has recently taken important steps in this direction, signing agreements with the Polish company ORLEN to supply 300 million cubic meters of natural gas to Ukraine from Polish LNG terminals on the Baltic Sea via the Polish gas transmission system. These being right steps by a state-owned company, it is necessary to move forward and independently cooperate with LNG producers and sign long-term contracts (up to 2 billion cubic meters per year) to obtain more favorable terms. Given the significant volumes of imports required, this is entirely logical.

Infrastructure challenges: bottlenecks and new opportunities

Technically, Ukraine has a guaranteed capacity to import 58 million cubic meters of gas per day from Europe via the following directions: 5.15 million from Poland, 9.76 million from Hungary, 42 million from Slovakia and 1 million cubic meters from the Trans-Balkan direction (Moldova) per day. In theory, neighboring operators can offer additional non-guaranteed capacity, but it is better to rely on the guaranteed one, which is sufficient to cover Ukraine's seasonal import needs.

However, in addition to technical capabilities, political risks and gas availability issues in these countries must also be taken into account. Slovakia offers the largest gas import capacity and is the optimal import route from Central European markets. Hungary currently offers attractive gas prices, but there is a risk that some of this gas may originate in Russia, as this country currently receives significant volumes of Russian gas via Türkiye and Bulgaria. Furthermore, Ukraine's convoluted political relations with the pro-Russian governments of Slovakia and Hungary should be born in mind. We all remember Robert Fico's threats to stop gas transit to Ukraine. Therefore, the creation of diversified gas supply routes to Ukraine is a paramount national task.

Poland could therefore become an important strategic partner for Ukraine and a window to the LNG market. It already has a modern terminal in Świnoujście, which is constantly increasing its capacity, and at the end of 2027 or early 2028, a new floating LNG terminal (FSRU) with an annual capacity of 6.1 billion cubic meters is planned to be launched in Gdańsk. Together with the GIPL gas pipeline connecting Poland with the Baltic countries and the Baltic Pipe, Poland is a powerful hub with access to alternative gas suppliers and markets.

At present, however, guaranteed gas import capacity from Poland is limited to approximately 5.15 million cubic meters per day (about 1.88 billion per year), which is clearly insufficient for a leap in cooperation between the countries. At the same time, Ukraine has the technical capacity to receive 18 million cubic meters per day (6.6 billion per year) at the border, but the Polish GTS is currently unable to supply such volumes to the border with Ukraine and requires investment in the development of gas transportation infrastructure in Polish territory.

The main barrier to realizing this potential remains the lack of funding for projects to expand gas transmission infrastructure in Poland. Unfortunately, after several attempts, Polish and Ukrainian GTS operators were unable to secure any long-term commitments from traders during the latest capacity allocation auctions, without which it is impossible to secure investment in new compressor stations and gas pipelines on Polish territory. This is a typical European approach: without capacity booking for 10–15 years, no country will invest in new construction because it is long-term booking that guarantee the return on investment of the Polish GTS operator in new infrastructure. Ukrainian traders, including Naftogaz, have regrettably shown no interest in booking capacity on the Polish-Ukrainian border or in the future terminal in Gdańsk. Therefore, Poland has not yet decided to develop gas transportation infrastructure to the border with Ukraine.

In my opinion, this is a strategic mistake on Ukraine's part, which deprives us of the opportunity to import additional gas volumes from Poland in the future. In addition, the lack of a strong connection with Poland will make Ukrainian underground gas storage facilities less attractive to Western traders.

Recommendation: chart a proactive strategic course towards long-term partnerships

We must move away from hotfixing existing problems (emergency gas purchases at any price) to more strategic planning and development. This requires building long-term alliances and mutually beneficial cooperation.

Right now, we need to, firstly, decide to reduce our dependence on gas imports through Slovakia and Hungary, and actively develop a gas supply route through Poland with direct access to Polish LNG terminals.

Secondly, long-term (3–5 years) contracts for LNG supplies should be concluded, primarily with the US, to ensure stable and competitive prices for imported gas.

Thirdly, new pipeline infrastructure and LNG terminal capacities in Poland should be booked in the long term to enable their use. This will significantly strengthen Ukraine's gas security and increase the attractiveness of Ukrainian gas storage facilities.

Ukraine faces new energy challenges that require the creation of strategic partnerships, long-term contracts and integration with the European market. Poland is not only a transit country but also a real energy bridge between Ukraine and the West. Ukraine's proactive stance will determine whether our country can ensure its energy security, become part of the European energy community and attract investment for economic recovery and development.

Now is the time for decisive strategic steps. Ukraine must not only respond to challenges but also shape its own energy policy focused on long-term stability, independence and prosperity.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google