Financial and Economic Policy in Wartime

article by Kyrylo Shevchenko, Ukrainian banker and the Chairman of the National Bank of Ukraine

Since the outbreak of Russia’s full-scale assault, the economy and financial system have shifted from operating on market-driven principles to being “manually” managed to meet unprecedented challenges. This approach has worked. It has helped alleviate panic and stabilize the financial and economic system.

However, as the economy has gradually recovered, the adverse and destabilizing effects of the financial system’s manual operation and the huge budget deficit have become more pronounced. This dictates the next stage in financial and economic policy: a transition to an acceptable budget deficit with market-based sources of funding. This transition will create preconditions for a return to traditional monetary instruments and market principles of the FX system’s operation.

The manually controlled mode of operation works well only during a significant psychological shock and the predominance of basic needs in the behavior of households and businesses.

The current model of managing the financial system is actually driven by three conflicting principles:

- The monetary financing by the NBU of most of the budget deficit is fueling depreciation and inflationary pressures.

- The Ministry of Finance is maintaining the yield on hryvnia government bonds at a low level, which falls short of covering inflation, stimulates consumption (i.e. increases inflationary pressures), and incentivizes the flow of savings into foreign currency (raising depreciation pressures).

- The NBU’s fixing of the exchange rate and tightening of the FX restrictions have enabled it to curb this depreciation and inflationary pressure.

The short-lived success of the manual mode has come at a price:

- Harsh restrictions on the movement of capital (FX restrictions, withdrawal limits, the ban on free movement of capital) and low interest rates on domestic government debt securities are being financed by holders of hryvnia savings and income, which are depreciating rapidly.

- The fixing of the hryvnia exchange rate is being financed with the NBU’s international reserves and exporters’ revenues. It is also making exporters and domestic producers less competitive relative to importers.

- Tax cuts are being offset primarily by monetary financing from the NBU (and therefore by an inflation tax that is being levied on all those using the hryvnia) and international loans and grants.

The economy is now gradually adjusting. Economic incentives are beginning to replace the psychological shock from the outbreak of the war and the predominance of charitable motives. Businesses aim to maximize their profits as households try to increase their incomes and protect their savings.

Such a change in the psychology of companies and individuals must be taken into account by economic policy makers. It is therefore necessary to gradually switch to more market-driven mechanisms, as running the economy in manual mode could cause a number of problems in the long run:

Problem 1. Dollarization and withdrawal of savings from the financial system. Holders of hryvnia savings are taking losses as the low return on bank deposits and domestic government debt securities, compared to the rate of inflation, erodes the real value of hryvnia savings. To protect their savings, households have therefore been withdrawing them from the financial system and exchanging them for FX cash (or transferring them to their cards abroad, or buying imported goods, or using hryvnia cards to make large purchases abroad). This is triggering what is known as the hot-potato effect, a situation where each new owner of a depreciating currency tries, as fast they can, to exchange it for another currency or commodity. And the faster the money circulates, the faster inflation will accelerate.

Solutions. First, the Ministry of Finance should increase the yield on hryvnia domestic government debt securities. It will also indirectly contribute to the growth in interest rates on deposits. The current growth rate of consumer prices (16.4% in April and 17% in May, by NBU estimates) and the forecast growth in consumer prices (20%+ until the end of 2022) remain important benchmarks for determining the necessary yield. This decision will stem hryvnia inflows into the FX market and ease depreciation pressures.

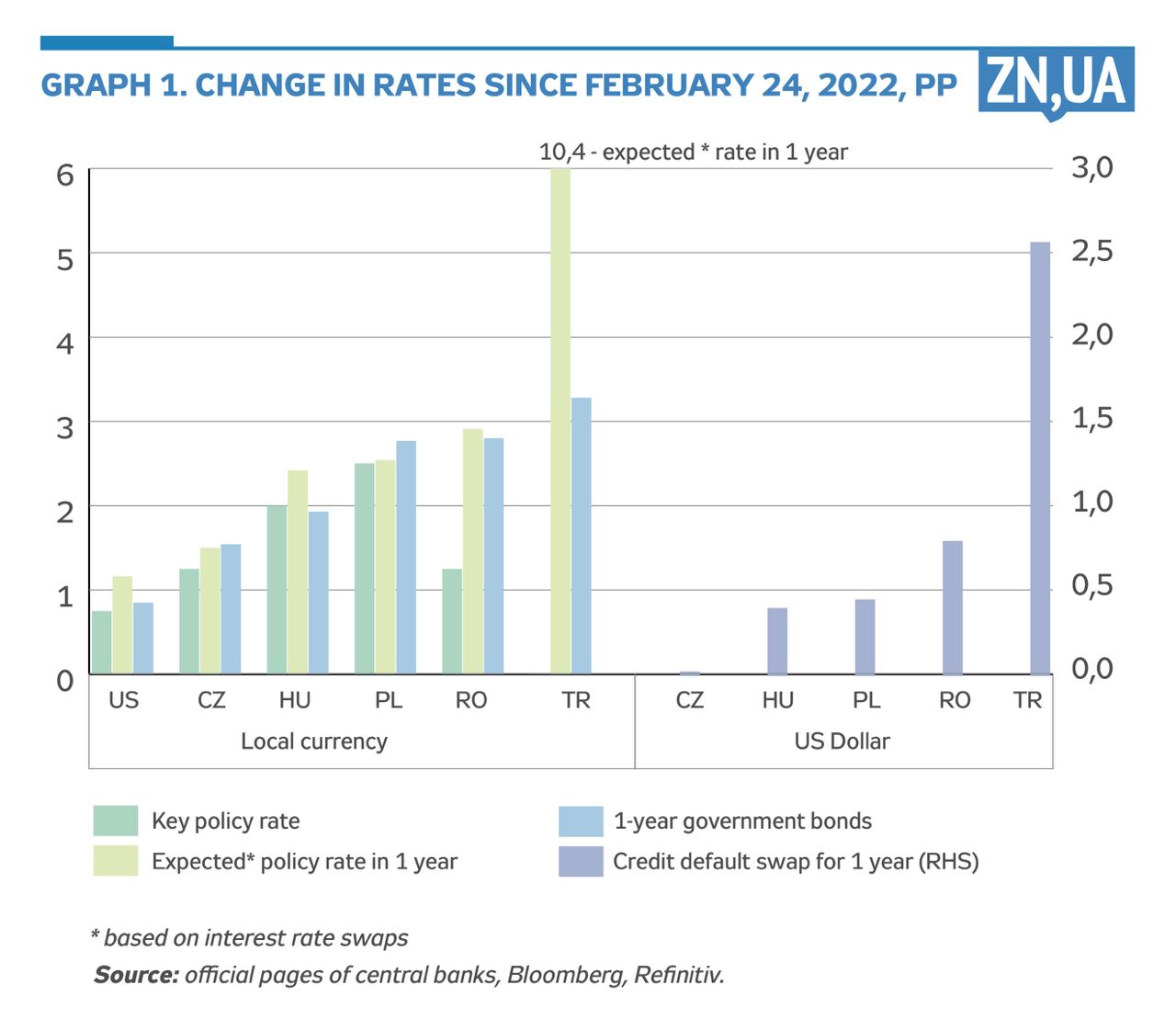

The increase in inflation is currently a global problem. Central banks in most countries (including the United States, the United Kingdom, Poland, and the Czech Republic) have been raising their key policy rates. Furthermore, yields on government securities around the globe have surged in recent months, primarily reflecting a response to the permanent acceleration in inflation, elevated geopolitical risks, and the slowdown in fiscal consolidation. This has been happening in countries with no active hostilities.

Watching a cat close its eyes as it laps up milk gives the impression that it is doing so to avoid seeing a world full of threats and being distracted from the main task. Unlike the cat, we cannot afford to have our eyes shut, because even a temporary misunderstanding of the situation can have dire consequences.

The NBU will eventually also have to “unfreeze” its key policy rate decisions and return to the pursuit of an active interest rate policy. Compared to prewar times, such an interest rate policy may be more focused on maintaining the exchange rate, given the stabilizing role it has been playing during the war.

Under such conditions, it is important that yields on domestic government debt securities respond to relevant changes in the key policy rate. It probably is currently the most important part of monetary transmission, i.e. the management of the financial and economic processes underlying the interest rate policy. Without an adequate response from interest rates on domestic government debt securities, it will be very difficult to manage the decisions of banks, businesses, and individuals as they choose a currency in which to keep their savings.

Problem 2. Decreased competitiveness of Ukrainian producers due to lower import taxes. In the early stages of the invasion, there were fears of significant disruptions of production in Ukraine because of hostilities. Given the potential need to replace domestic production with imported goods, cutting import taxes was the right move. Fortunately, the manufacture of consumer goods has survived and is primarily recovering in relatively quiet regions. This also applies to the production of goods designated for export. However, the import incentives created through the abolition of import duties and VAT are now depriving Ukrainian businesses of a competitive edge.

Solutions. It is necessary to reinstitute import taxes and impose an additional import duty on noncritical import categories. This will boost budget revenues, reduce imports, and stimulate Ukrainian producers, thus easing the pressure on the FX market. This will also alleviate the need for the NBU to finance the budget deficit and will therefore relieve depreciation and inflationary pressures.

The NBU has repeatedly addressed the Cabinet of Ministers with relevant proposals, and, given the constructive dialogue on import taxation, we hope that these decisions will be passed by the Verkhovna Rada in the near future.

Raising import taxes and the yield on domestic government debt securities will enable a gradual transition to a floating exchange rate regime whereby the NBU will smooth out exchange rate fluctuations without fixing the exchange rate itself. However, to make sure that this transition is as smooth as possible, without sharp fluctuations or shocks taking place, and that the exchange rate can go up and down like it did before the war, the FX market must be able to self-balance. This capability will primarily be facilitated by the growth in export supplies as logistical hurdles are resolved and the monetary financing of the budget is phased out (more on this below).

Another option is to withdraw from the interbank FX market any large public sector buyers whose imports are inelastic with respect to the exchange rate, meaning the buyers that do not decrease or increase their imports when the exchange rate changes.

For instance, import purchases by the Ministry of Defense and the Ministry of Health and large state-owned companies in the defense and energy sectors can be made with the foreign currency sold by the NBU at a fixed exchange rate. The central bank will buy it from the Ministry of Finance at the same rate.

Problem 3. Shadowization of the economy to circumvent restrictions, which is evidenced in particular by cash exchange rate movements. Pressure on the cash FX market has been driven by the increase in the supply of hryvnias as the NBU has conducted the monetary financing of the state budget deficit. This is ramping up pressure on international reserves to decline and on the hryvnia to depreciate in the cash exchange segment and the card-based settlements segment, stirring up overall social tensions and discontent. To keep the exchange rate fixed, the NBU sold USD 1.8 billion in the FX market in March, USD 2.2 billion in April, and USD 3.0 billion in the first 27 days of May (for the whole of May, the figure will likely have risen even more). At the same time, in cash exchanges against the U.S. dollar, the hryvnia depreciated by 3% in March, by 4% in April, and by more than 9% during 1–27 May.

|

In equivalent of USD millions |

Sold by clients |

Bought by clients |

Net client transactions |

Net bank transactions through enforcement proceedings (“-” net purchases) |

Net NBU interventions |

|||

|

January |

6,821 |

8,122 |

-1,300 |

-13 |

-1,314 |

|||

|

February |

8,649 |

8,372 |

276 |

-584 |

-308 |

|||

|

March |

2,974 |

3,044 |

-70 |

-1,706 |

-1,776 |

|||

|

April |

2,903 |

3,146 |

-243 |

-1,960 |

-2,203 |

|||

|

May (as of the 27th) |

3,033 |

4,000 |

-968 |

-1,887 |

-2,855 |

|||

Solutions. The implementation of measures to resolve the first two problems will allow the NBU to gradually roll back the FX restrictions. This will help bring FX transactions out of the shadow, increase the circulation of foreign currency in the legal market segment, strengthen its stability, and eliminate the multiplicity of exchange rates.

Problem 4. Loss of confidence in the hryvnia due to monetary financing and the lack of ability to control the exchange rate in the cash market. The NBU is currently “printing” hryvnias to meet the bulk of the budget deficit through monetary financing. This is generating depreciation and inflationary pressures.

|

Breakdown of hryvnia issuing and withdrawal, UAH billions |

February |

March |

April |

May |

February–May |

|

FX purchases from (-)/sales to(+) the NBU by the government |

-8.6 |

40.1 |

57.9 |

65.2 |

154.6 |

|

Transfer of NBU profit |

18.8 |

0.0 |

0.0 |

0 |

18.8 |

|

NBU net transactions with domestic government debt securities |

-1.3 |

19.4 |

48.9 |

34.4 |

101.5 |

|

Net refinancing of banks |

38.9 |

-6.5 |

-5.9 |

-10.6 |

15.9 |

|

NBU’s “monetary injections” |

47.9 |

52.9 |

100.9 |

89.0 |

290.7 |

|

NBU interventions to purchase (-)/sell(+) |

9.0 |

52.2 |

65.1 |

88.2 |

214.5 |

|

* Redemption by the NBU of military domestic government debt securities (+)/redemption of and income from government securities (-) in the NBU portfolio |

|||||

This pressure has been partially restrained by fixing the cashless exchange rate and tightening the FX restrictions. To achieve this, however, the NBU has been drawing on scarce international reserves. This is eating away at confidence in the hryvnia’s strength and driving depreciation expectations higher.

Sales of international aid funds in the FX market are only partially addressing this problem, as this is primarily credit financing (borrowed at very low, nonmarket interest rates) that will have to be repaid. As a result, expectations for the future will not improve.

The longer these imbalances are allowed to accumulate, the greater the loss in the hryvnia’s value, and the longer it will take to restore confidence in the domestic currency. All else held equal, such conditions will require higher interest rates and a longer application of FX restrictions going forward. This will constrain the economic potential.

Problem 5. The vicious cycle of state budget problems will only expand:

- The reduction in tax revenues due to the shadowization of and pressure on Ukrainian-based producers.

- The inability to ensure the market-based financing of the budget with hryvnia funds. Demand for hryvnia domestic government debt securities is weakening due to depreciation and inflation risks. Domestic government debt securities with artificially low yields are unprofitable for the holders of these assets, which will fall in price if the hryvnia depreciates. As a consequence, the Ministry of Finance will still be forced to raise the yields, but this increase may grow in significance. In addition, it is impossible to rely solely on monetary financing from the NBU, as this puts the FX market under additional pressure.

- The high share of FX public debt leads to the impossibility of finding a depreciation-and-inflation-based solution to the budget problems. The growth in revenues through inflation and depreciation will be offset by the need to index expenditures and increase the cost of servicing FX and indexed debts. Increasing the need for monetary financing only exacerbates the problems outlined above. Similarly, external assistance/borrowing is not addressing accumulated imbalances, but is only postponing the measures required to correct the macroeconomic mismatches.

Going forward, all of these problems will only get worse, leading to the need to make even more painful decisions in the near future. The tax base will shrink (as the domestic producer is suffering), and the hryvnia will lose the public’s trust, making it impossible to finance the budget by taking on more hryvnia debt in future periods.

The delayed need for significant tax increases and budget expenditure cuts will therefore only increase with time.

Ways to resolve problems 4 and 5:

Implementation of measures to resolve problems 1 through 3 will contribute to dealing with problems 4 and 5. However, in order for these measures to succeed, it is critical to implement them in phases.

First, it is necessary to return to the taxation of imports and the introduction of an additional import duty on noncritical categories of imports.

Second, it is important to introduce a fair reward for those investing their savings in hryvnia domestic government debt securities.

The next potential step is to remove large public-sector buyers from the FX market.

Only after that will it be possible to make a gradual transition to a floating exchange rate that must fluctuate in both directions. And this should be followed by a gradual rollback of FX restrictions.

The new program with the IMF should become an important element in maintaining macro-financial stability. In the earliest weeks of the war, any discussion of the new program was essentially hampered by the inability to develop a more or less reliable macroeconomic benchmark with a sufficient level of confidence. Fortunately, we are now at a point where the financial system and the economy have recovered from the initial shock and are shifting to a new mode of operation that takes into account specific wartime conditions. This leaves us with the need to reconfigure our economic policy controls. The IMF has traditionally specialized in helping countries with difficult financial and macroeconomic conditions. IMF loans will also be welcome.

Economic policy has come to a crossroads and has to choose between two alternatives:

One option is to maintain the current format despite threats of increased economic imbalances and the risk of an inflation-depreciation spiral. For the vast majority of Ukrainians, including those displaced and currently living abroad, hryvnia incomes and savings will seriously depreciate. A heightening of social tension and inequality will inevitably follow, because inflation is a tax paid by the poor. Owners of large assets, on the other hand, will benefit at the expense of the “average Ukrainian.” Disgruntled with the situation, however, the latter will probably choose to emigrate. As a result, long-standing problems, such as the “oligarchization” of the economy, the outflow of labor, and the brain drain, could get even worse.

The NBU is clearly opposed to a scenario in which ordinary people shoulder most of the burden of wartime problems by struggling with high inflation and seeing their hryvnia incomes and savings depreciate. At the end of the day, the classic inflation-depreciation spiral will have to be slowed and changes will have to be made in any case, but conditions will have deteriorated, meaning that these decisions will be more painful.

The other option is to return to the market principles of financial and economic system management, with an acceptable budget deficit and market sources of funding. Such steps will be unpopular, as hryvnia interest rate increases, for example, are usually not welcome, although lending is currently also severely limited by “nonmarket” factors. In addition, increases in import taxes have an adverse impact on importers, including domestic producers and consumers of finished products.

At the same time, decisions taken on time will ease the issues outlined above, relieve pressure on the financial system, in particular the domestic currency, and ease the transition from “manual” to market-based management, subject to wartime requirements. This will reduce existing imbalances and readjust the system to new operating conditions.

In his 1940 paper eloquently titled “How to Pay for the War,” John Maynard Keynes argued that it is imperative, first and foremost, to avoid inflation, which does not resolve the problem of financing the government’s war expenditures, but only deepens this problem, leading to social inequality. He highlighted the importance of avoiding financing the growing cost of war through inflation. He suggested that a part of consumption be delayed until after the war is over.

Read this article by Kyrylo Shevchenko in russian and Ukrainian.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google