Rapid Post-War Recovery: Is It Possible in Ukraine?

Lost Budget Revenues: Who Bears Most of the Blame

23 january, 2026, 11:28

Share

Taxes are the sinews of war.

— Thomas Sargent, Nobel laureate

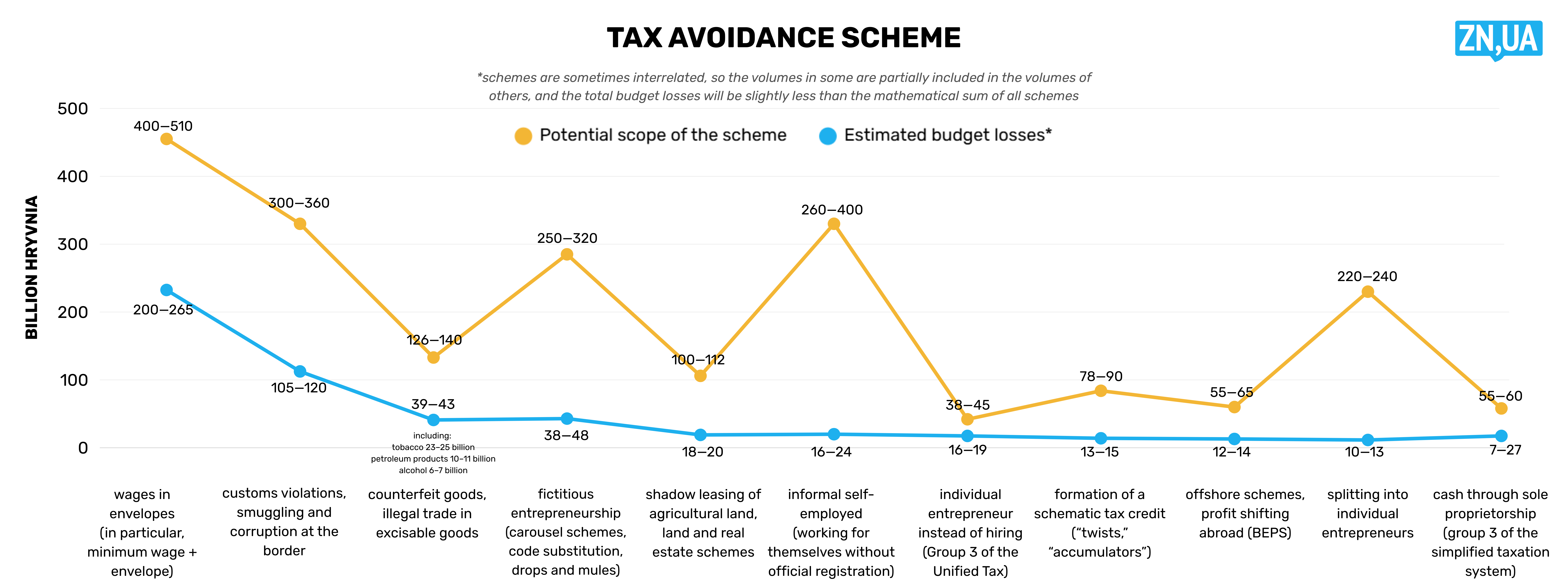

For the tenth consecutive year, a team of experts from the NGO Institute for Socio-Economic Transformation, CASE Ukraine, and the Economic Expert Platform has been working to find optimal ways to fill state coffers—primarily by closing the most widespread channels of tax evasion. According to their estimates, the structure and classification of the most common schemes, their scale and, crucially, the associated budget losses last year looked as follows:

ZN.UA

As the data show, the scale of the 11 most widespread tax evasion schemes is staggering: at least UAH 1.8 trillion annually, equivalent to 21.3% of GDP (GDP forecast for 2025: UAH 8.47 trillion). Potential annual budget losses are estimated at UAH 474 billion—around 15% of the projected revenues of the general fund of the national and local budgets for 2025 (preliminary estimate: UAH 3.17 trillion).

In other words:

- every fifth hryvnia in the economy is of illicit origin (i.e., involved in tax evasion);

- one out of every six hryvnias of budget revenue is lost.

Unfortunately, the bad news does not end there. The harsh and unpredictable tax policy proposed to society in recent years has had little to no effect—except in isolated cases—on most popular tax minimization schemes. Year after year, they either continue to grow or, at best, remain substantial. First and foremost, this concerns envelope wages, violations of customs rules, smuggling and corruption at the border, and counterfeit goods and illegal trade in excisable products.

ВАС ЗАИНТЕРЕСУЕТ

Notably, the “shadow wages” scheme emerged as the single largest source of fiscal losses last year, with estimated annual losses of UAH 200–265 billion.

The dynamics of tax evasion through customs violations, smuggling and corruption at the border also remain alarming. Discrepancies in mirror customs statistics (comparisons between partner countries’ data and national customs records) reached a record $17.24 billion in 2024 ($14.67 billion in 2023). At the same time, in-depth analysis of 13 high-risk imported goods categories—accounting for 17.51 percent of total imports in 2023 (including smartphones, batteries, footwear and vehicles)—revealed value gaps totaling $1.13 billion, which represent a potential tax base lost at the border.

Another widespread instrument of tax evasion at the border is the abuse of tax exemptions provided by treaties and domestic tax legislation. This includes importing commercial consignments disguised as postal or courier shipments, which benefit from an exemption (goods valued up to €150 are not taxed) and simplified declaration and clearance procedures.

Cross-border marketplaces whose business models rely on exploiting this exemption enjoy significantly more favorable fiscal and regulatory conditions than official importers and domestic producers. According to existing estimates, had parcels valued up to €150 been subject to taxation, additional VAT revenues alone would have reached UAH 17.8 billion last year. If the exemption is abolished this year and current growth rates of international postal and express shipments persist, Ukraine could expect up to UAH 27 billion in additional budget revenues.

As a result of the full-scale war and related measures, some schemes—including what was once the largest channel for cross-border profit and capital shifting via offshore zones—have significantly diminished. Wartime regulations and international efforts to enhance tax transparency have left them far less room to operate. The number of informally employed workers has declined due to the overall contraction of the labor force. The share of large businesses has likely decreased as well, owing to destruction and the temporary occupation of territories that traditionally hosted major industrial enterprises.

At the same time, the needs of the economy—particularly its grey and black segments—for cash, the necessity of circumventing financial monitoring restrictions and currency controls, and the provision of services related to falsifying or manipulating primary documentation and tax invoices have created conditions in which “domestic-use” have emerged as the dominant form of tax evasion. As the simplified tax regime has been progressively narrowed, these schemes have migrated into the general tax system.

This is precisely why the past two years have seen a renaissance of fictitious entrepreneurship, notably the industry of transit-and-cash-conversion centers and schemes involving “drops” or “mules.” These have surged to UAH 250–320 billion per year (the National Bank of Ukraine estimates the activity of a single “drop” at up to UAH 2.5 million annually). The scale of these schemes directly depends on corruption within law enforcement, supervisory and regulatory bodies.

Overall, assessing the state of countermeasures against the most widespread tax evasion schemes in 2023–2025 leads to an unpleasant conclusion: the state’s efforts have been at best misdirected. Pressure has been applied almost exclusively to the formal sector of the economy—“white” wages and passive household incomes (including the 5 percent military levy), legal bank profits (subjected three times to an extraordinary 50 percent tax rate), as well as entrepreneurs and small businesses. At the same time, tax policy has inexplicably avoided confronting the two shadow titans—off-the-books wages and smuggling—which together account for nearly 65 percent of all potential budget losses. A striking blindness. Each of these shadow titans could, on its own (and sometimes multiple times over), fully replace, for example, revenues from “VAT for taxpayers using the simplified regime.”

Thus, Ukraine’s current tax policy remains severely and chronically ill, while the remedies applied either do not work (producing no tangible effect) or treat the wrong diagnosis (focusing on less urgent problems).

At the same time, the most promising steps to reduce the shadow economy and decisively increase budget revenues most likely lie in a radical reboot of state institutions:

- Customs Service: the process has just begun, but if successful, it could lead to a radical reduction in smuggling and gray imports;

- Tax Service: rebooting remains “not the time,” as the government persistently ignores the issue, and parliament has yet to consider it (Draft Law No. 9243 has been pending since April 2023);

- Economic Security Bureau (ESB): there is hope that after a successful reboot in 2026 (the personal composition of attestation and staffing commissions was approved only two months ago), systematic action against VAT fraud schemes, envelope wages, counterfeit goods and grey excisable trade will finally gain traction and eventually put an end to these practices;

- Ministry of Finance: the institution responsible for fiscal dialogue with the IMF and the accumulation of most radical innovations that provoke business backlash.

ВАС ЗАИНТЕРЕСУЕТ

That is why Ukraine urgently needs:

- institutional reboots;

- an honest audit of its excessively complex, bloated, unstable and business-hostile tax legislation, including a reduction of tax exemptions (of which there are more than 260);

- a change in the tax policy course, its demilitarization vis-à-vis taxpayers.

And most importantly, there must be enough time and political will to make all this happen.

Noticed an error?

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Stay up to date with the latest developments!

Subscribe to our channel in Telegram

Пожалуйста выберите один или несколько пунктов (до 3 шт.) которые по Вашему мнению определяет этот комментарий.

Пожалуйста выберите один или больше пунктов

Нецензурная лексика, ругань

Флуд

Нарушение действующего законодательства Украины

Оскорбление участников дискуссии

Реклама

Разжигание розни

Признаки троллинга и провокации

Другая причина

Отмена

Отправить жалобу

ОК

Login with Google

Login with Google