Will Dollar Cost 45 UAH... And Other Issues That Concern Everyone

What should Ukrainians expect: a new devaluation spiral, a new exchange rate “shelf” or an exchange rate correction that will take place over time? Let’s try to figure it out.

The Ministry of Finance needs a “45 UAH exchange rate”

Currently, the main budget-forming taxes in Ukraine are personal income tax and taxes collected by the customs service (import duties, VAT and excise taxes on imported goods). It is clear that the latter types of budget revenues directly depend on the official exchange rate of the hryvnia against the dollar and the euro, as they are calculated from the contract value of the goods in foreign currency and the official exchange rate of the National Bank of Ukraine (NBU) on the day of customs clearance.

In the second half of 2024, Ukraine may receive an average of UAH 50 billion per month in customs payments from the customs service. A 10% devaluation of the hryvnia, for example, means an additional UAH 5 billion in additional tax revenues per month or UAH 30 billion for the first half of the year (which is 30% of the government’s plan to “find” approximately UAH 100 billion by increasing taxes by the end of the year).

If the depth of devaluation is 20%, it will imply an additional UAH 60 billion from customs.

Given the goals of the budget policy and the need to keep the budget deficit within the planned horizon, the Ministry of Finance needs a “45 UAH exchange rate.”

However, the NBU realizes that such a sharp devaluation could lead to people withdrawing funds from demand accounts (mainly card accounts) and deposits, which will then be converted into dollars.

“Freezing” people’s money in banks to stabilize the exchange rate in this case is also an unacceptable scenario, given the extremely toxic consequences of such a development.

So far, this trend has not been observed: at the beginning of the year, households’ funds in banks amounted to UAH 1,083 trillion, including demand deposits of UAH 694 billion, or 64%. In the first half of 2024, these figures increased to UAH 1,123 trillion and UAH 719 billion, respectively.

However, the extremely high level of household demand deposits is noteworthy: almost two-thirds of the total amount of household deposits is in banks.

What will the NBU do?

In monetary policy, there is a kind of “impossible trinity” of international finance: it is impossible to fix the exchange rate, conduct sovereign monetary policy (change the discount rate), and ensu discount rate re free capital flows at the same time. Only two of the three options can be chosen at the same time.

In the first months of the war, the NBU opted for what can be conveniently called free capital flows (despite certain restrictions, the foreign exchange market functioned, especially the cash market) and a fixed exchange rate, while refusing to change the discount rate (fixing it at 10%).

The NBU then tried to choose all three options of the impossible trinity, albeit in a hybrid form: the key policy rate became mobile (it was raised to 25% in June 2022); capital flows were further liberalized in the fall of 2023; and the fixed exchange rate policy continued until October 2023.

As we can see, the history of the hryvnia exchange rate during the war has three main stages (see Figure 1).

.png)

The first was fixing the exchange rate at 28.98 as of February 23, 2022. Very soon, this rate broke away from the cash rate and the gap was up to 20%.

The second stage was a period of “manual” adjustment of the exchange rate, when on July 22, 2022, it was transferred to the 36.56 echelon and remained at this level until September 30, 2023, when a “quasi-market rate” was introduced and partial liberalization was carried out during the war.

It was a very risky step because in wartime, the uncertainty factor plays an unacceptably large role, and any negative events at the front or in the rear can cause panic among the population and, consequently, high exchange rate turbulence.

However, the more or less stable autumn period even led to a certain appreciation of the hryvnia to 36.04 in November last year, which looked rather atypical at the time.

The third stage is in fact a conditional “free float” of the hryvnia under the watchful eye of the whistle-blowing coach, the NBU.

The gradual devaluation of the hryvnia began in March 2024 and continues today. However, certain panic moods have not yet spread in the foreign exchange market, perhaps due to the fact that the “hryvnia exchange rate issue” is less important than other current existential challenges for Ukrainians.

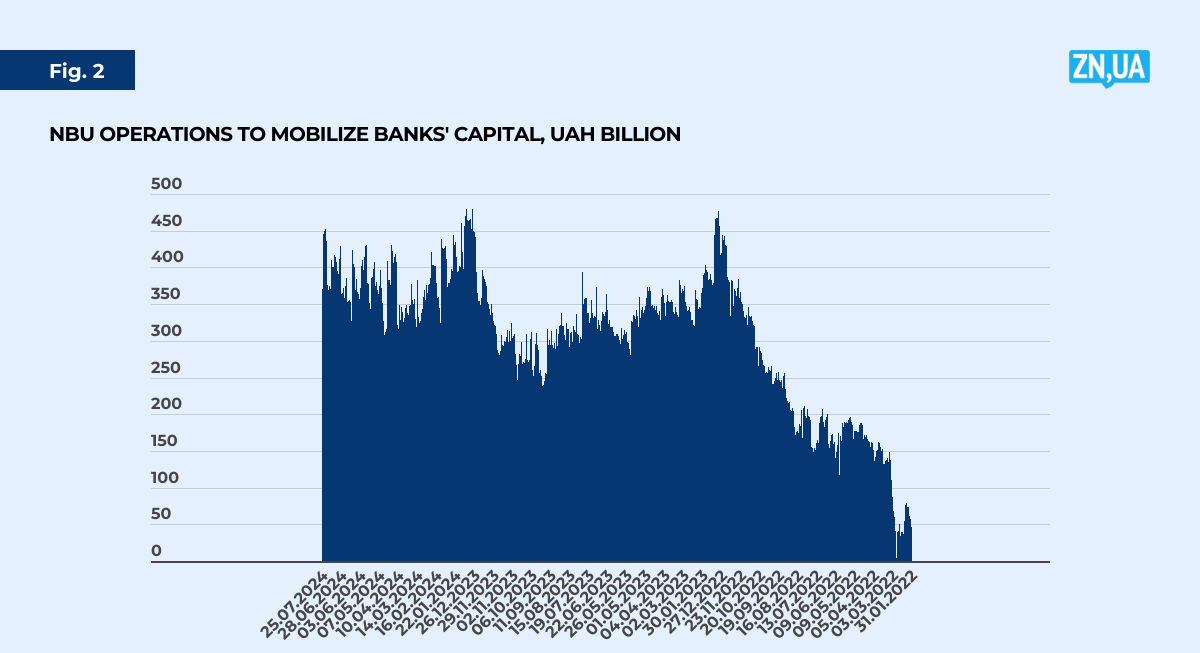

Exchange rate stability over the entire period was ensured, among other things, by a significant withdrawal of temporarily free liquidity from banks (immobilization of funds in NBU certificates of deposit). As can be seen in Figure 2, after such withdrawals peaked at almost UAH 500 billion at the end of 2022, the amount of bank liquidity withdrawn from the economy began to decline slightly, and funds gradually started to flow into the real sector (although this process was very slow).

Nevertheless, the amount of immobilized liquidity declined from the extremes of UAH 466 billion at the end of 2022 to UAH 230 billion in the fall of 2023. However, currency liberalization gradually took its toll: the volume of immobilization began to grow rapidly again, along with the process of exchange rate liberalization and further hryvnia devaluation, reaching new highs of UAH 450–460 billion this year.

During the war, the balance of bank customers’ foreign currency transactions amounted to minus $25 billion. This year, compared to last year, this figure increased by 19%, and by 47% compared to the year before.

Instead, individuals’ foreign exchange balances amounted to minus $10.7 billion during the war, with cash transactions dominating this structure at 85%.

In other words, the main pressure on the hryvnia in the context of transactions by individuals comes from the cash market.

If we compare the first half of 2022, 2023, and 2024, we get the following figures for the balance transactions of clients of foreign currency tanks: "plus" 0.7, "minus" 1.8, and "minus" 5.24 billion dollars. Compared to the previous year, this figure increased by 177%, and by 836% the year before that.

Please note that the negative balance of transactions of individuals in the first half of 2024 is almost half of the total negative balance for the entire period of the war.

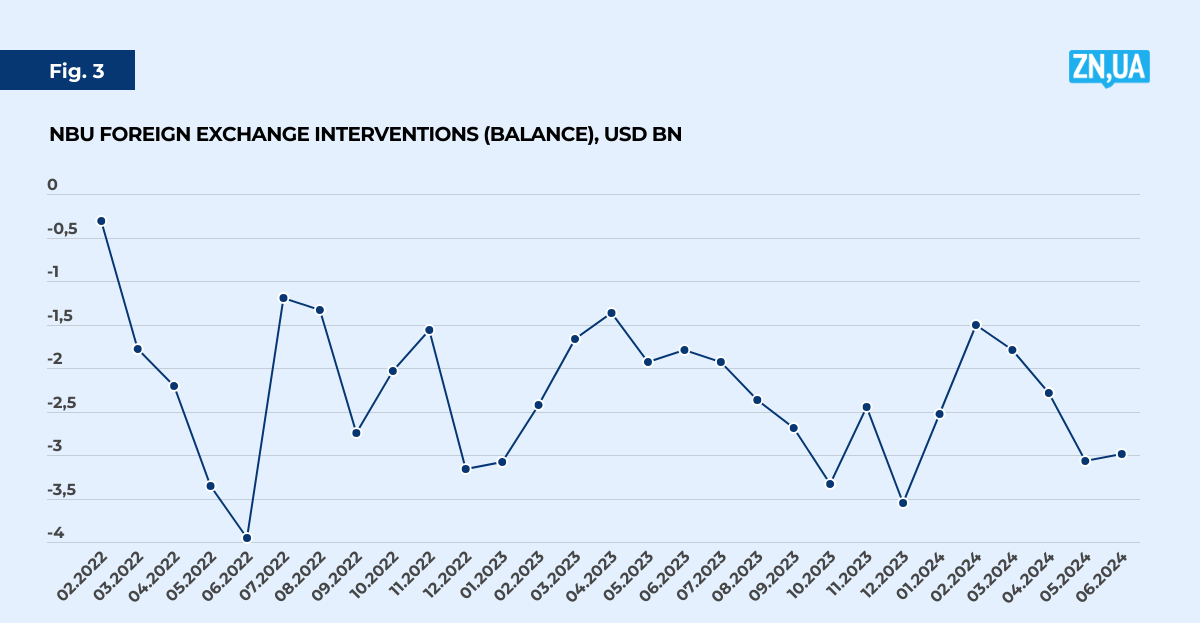

To dampen exchange rate peaks or troughs, the NBU increased the volume of its FX interventions (see Figure 3).

In total, during the war, the balance of the National Bank’s operations to support the hryvnia exchange rate amounted to $66.41 billion. The NBU bought only $3.53 billion over 2.5 years, but sold almost $70 billion of its own foreign exchange reserves on the market. Given the average size of foreign exchange reserves at $40 billion, it is clear that the stability of the hryvnia exchange rate is a derivative of the amount of external financial assistance rather than of the NBU’s policy.

According to the Ministry of Finance, in 2022–2023, Ukraine received $73.5 billion in financial assistance from Western partners. Another $16 billion was received in the first half of 2024. The total amount is $89 billion. These funds have become part of not only the foreign currency account of the Ministry of Finance, but also the NBU reserves (the budget is financed in hryvnia).

We already know that $66.41 billion was used to cover the NBU’s negative balance of operations in the foreign exchange market. Where did the other $22.6 billion go? The difference was used to increase the NBU’s foreign exchange reserves, which grew from USD 25 billion at the beginning of the war to USD 43 billion in March of this year, i.e., by $18 billion. The rest was spent on foreign currency payments by the government and the NBU, including debt repayments.

However, starting in March of this year, the NBU’s foreign exchange reserves began to decline, and now amount to almost $38 billion ($26.3 billion in net reserves), meaning that in March–June 2024 alone, the NBU lost almost $5 billion in reserves, or 11%.

It is worth noting that the trend toward hryvnia devaluation began in March 2023, and the NBU’s foreign exchange interventions have again reached their peaks: now the reserves are being “burned” almost as much as in the summer of 2022 and late 2023: about $3 billion a month.

***

The devaluation of the hryvnia is not related to business activity or import growth compared to other periods of the war. Instead, there was a strong outflow of currency through the cash market and household transactions. This coincided with a negative information flow.

Under these conditions, the NBU’s foreign exchange interventions are limited to USD 3–4 billion per month, which will slow down the “burning” of reserves, but will not stop the devaluation.

Last fall’s currency liberalization in the midst of the war seems to have been a mistake, as the uncertainty factor has not disappeared and the planning horizon is still low. The NBU will save the use of reserves and increase the withdrawal of hryvnia from circulation by issuing certificates of deposit. This, however, will be detrimental to economic recovery.

The struggle between the two desired exchange rates, 40 UAH for the NBU and 45 UAH for the Ministry of Finance, will lead to a compromise rate in the range of about 41–43 UAH per dollar.

In case of a reduction in external support or a delay in its receipt, the exchange rate may drop to 45.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google