How About We Talk It Through? Absent Efficient Communication, Don’t Expect Stability

The persistent uncertainty increases the risks that affect the exchange rate, inflation and economic growth. These risks are largely beyond the central bank’s control, which means that the impact of monetary instruments on inflationary processes, including the economic situation in general, is currently significantly limited. How can inflation be curbed by raising excise duties or taxes? How can we prevent the growth of pessimistic inflation expectations if the government reports a “half-a-trillion-hryvnia hole in the budget”?

Nevertheless, in the end, the burden of responsibility for the risks that have materialized, both inflationary and exchange rate ones, will, according to the law, rest squarely on shoulders of the regulator.

For example, while the National Bank of Ukraine (NBU) can restrain sharp exchange rate fluctuations through its own interventions in the foreign exchange market, it can only influence expectations indirectly through communications with society. The main principle of the central bank should now be “talk the walk and walk the talk.” This is an important prerequisite for further ensuring macroeconomic stability. However, it is desirable that other macroeconomic agents, such as the government and the parliament, always adhere to this principle.

On July 24, the NBU Board decided not to change the key policy rate and to keep it at 13%. On August 1, the NBU released its July Inflation Report. And on August 6, the NBU held a meeting with a wide range of economic experts to discuss the next monetary decision on the key policy rate and other monetary measures, as well as the NBU’s new macroeconomic forecast. All of these measures are carried out in line with the NBU’s strategy of transparency and accountability through a thorough and extensive system of communications with the government, experts, business and the public.

At the same time, there were no other public communications or strategic planning of government decisions by other branches of government that could also influence inflation to curb it, and thus the economic situation...

This should be worrisome, as it adds to the uncertainty that is already present. After all, economic policy is a team sport, and no matter how strong one attacker is, he or she still relies on the coordinated work of other players. And inflation, although legally within the NBU’s purview, is also influenced by fiscal policy or legislative changes and affects the entire economy and the entire population.

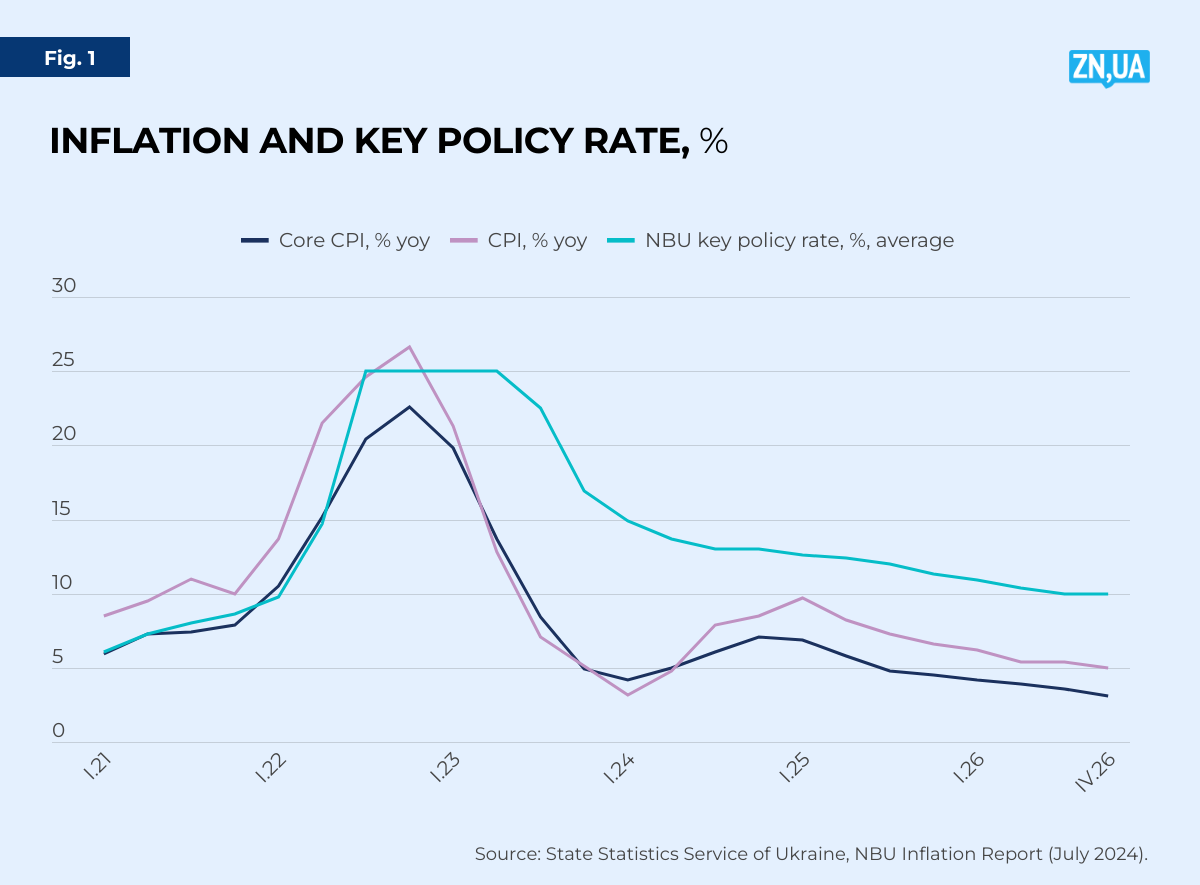

Let’s delve into the inflationary details. The NBU has raised its inflation forecast to 8.5% by the end of the year. That is why the NBU suspended its key policy rate cuts and kept it at 13%. Despite the relatively low level of current inflation in July at 5.4%, the downward trend reversed in May. Demand-pull inflation also began to rise, pushing core inflation up to 5.7% in July (see Figure 1).

Fundamental pressures intensified due to higher business costs for higher wages and electricity costs, as well as the effect of the hryvnia devaluation being passed through to price increases. The NBU expects further strengthening of the fundamental factors on the demand side of inflation, which will be reflected in an acceleration of core inflation by the end of the year. According to its forecast, core inflation may reach 7% by the end of the year.

The government’s decision to raise taxes could also become a significant inflationary factor. Obviously, these additional budget revenues will immediately go to the military and will quickly boost demand in the consumer market.

At the same time, the pressure on inflation may increase due to a decrease in the supply of vegetables and other raw food products due to the hot weather this summer.

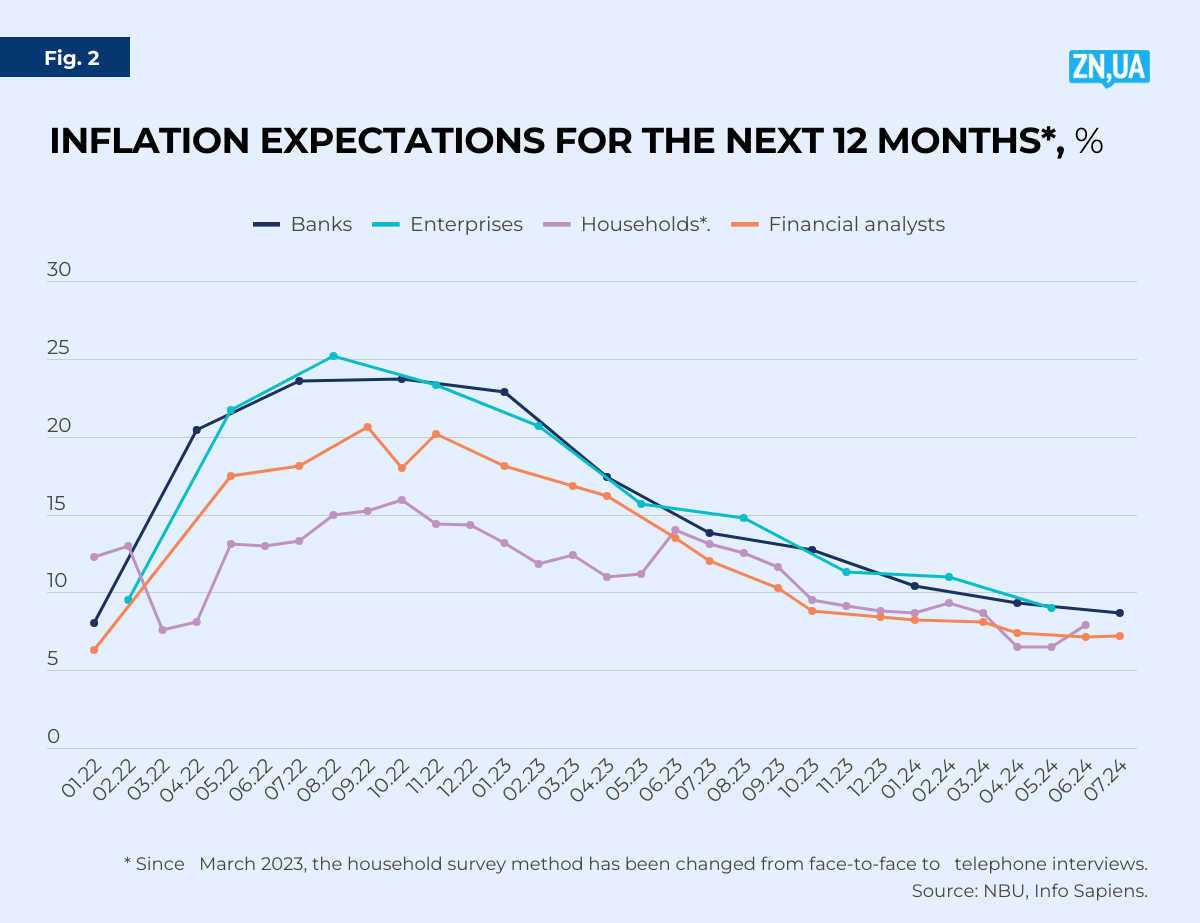

All of these pro-inflationary factors have contributed to a deterioration in inflation expectations among households, which are gradually beginning to respond to the change in the inflation trend (see Figure 2).

It is clear that the NBU’s decision to keep the key policy rate unchanged was influenced by its desire to keep household and business deposits in hryvnia attractive, i.e. at a positive level relative to future inflation. This decision, on the one hand, counteracts the flow of hryvnia from deposits to the foreign exchange market, and on the other hand, protects hryvnia savings from inflation. Of course, such a decision will to some extent slow down lending due to high interest rates, although the main factors behind high lending rates are all the risks associated with the war.

However, starting in mid-2025, inflationary pressures should ease thanks to the NBU’s measures and an improvement in the energy supply situation. The NBU estimates that inflation will be 6.6% by the end of 2025.

How will all this affect the economy? The NBU estimates real GDP growth at 3.7% by the end of the year.

Of course, even such an economic growth rate is positive in a time of war, although it should be borne in mind that it is calculated from a very low comparison base, when the real GDP decline in 2022 was 29.1%. After a sharp jump at the beginning of the year, real GDP growth slowed significantly due to a precipitous drop in electricity supply, which was due to the destruction of our energy and infrastructure facilities by the Russians.

Due to the extensive damage to production facilities and infrastructure, exports of metallurgy and machine building products will be weak, and the dynamics of exports will be determined by the level of agricultural harvest. On the other hand, the expansion of export routes amid a rebound in external demand will contribute to growth.

In its forecast, the NBU assumes a harvest of 54 million tons in 2024 and 58 million tons in 2025. At the same time, the current account deficit will worsen in 2025 (minus $19 billion versus minus $14 billion in 2024).

At the same time, the same current fiscal policy and, accordingly, significant public spending will be the main driver of economic growth in 2024.

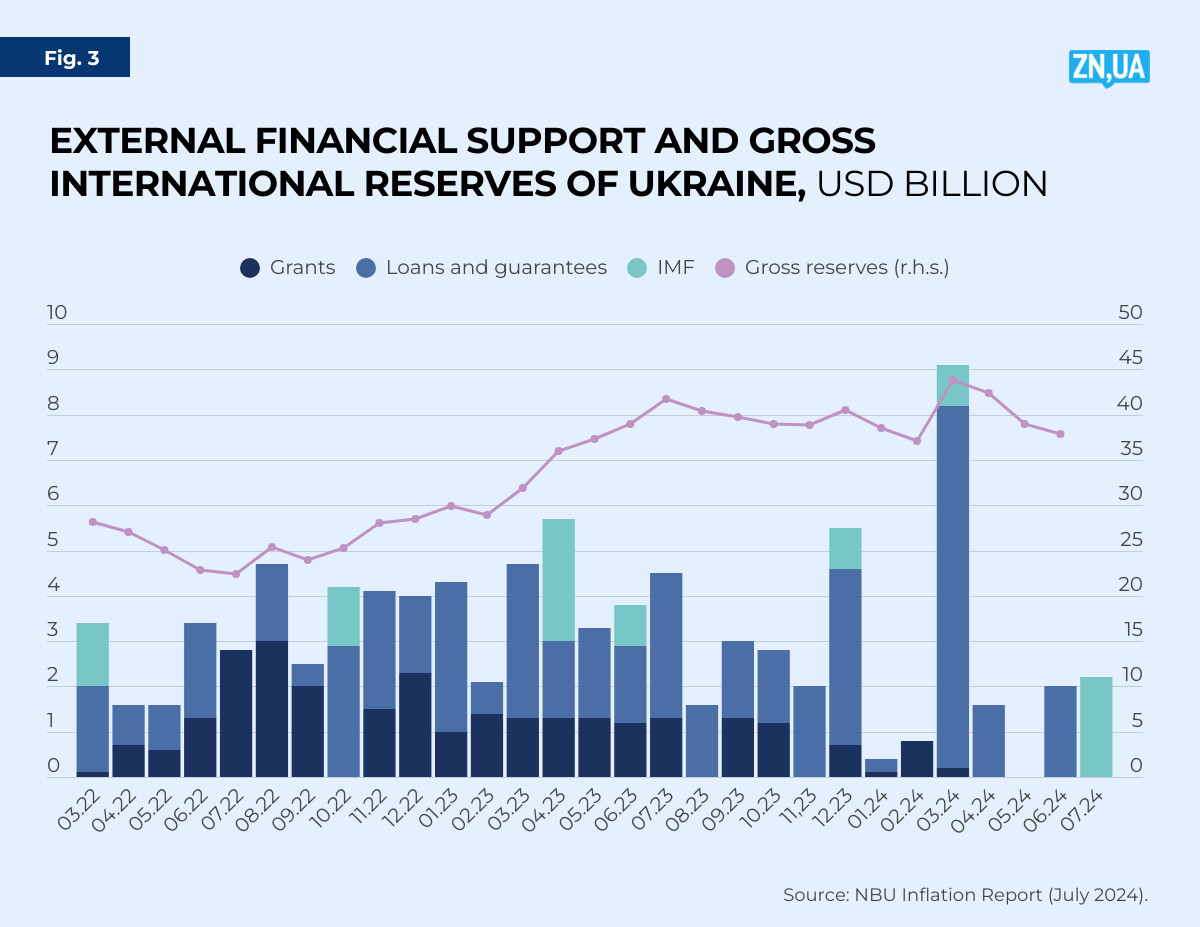

As of August 1, the level of international reserves stood at $37.2 billion. The NBU expects that the downward trend in international reserves will gradually decline by the end of the year, and that their level will remain sufficient to ensure the stability of the FX market (see Figure 3).

Many politicians and experts are of the opinion that the NBU has too many foreign currency reserves on its balance sheet, and that some of them could be used for the needs of the economy and defense. However, both the Ukrainian experience of the 2008 crisis and the experience of other countries have shown that the sufficiency of foreign exchange reserves is a major safeguard against currency crises and a factor in ensuring macroeconomic stability.

Currently, the level of international reserves exceeds 100% of the minimum required by the IMF’s composite criterion, but this IMF criterion for reserve adequacy is calculated for countries that are not in a state of war. Instead, the role of reserve adequacy for Ukraine, which is in a state of war and, accordingly, in conditions of high uncertainty, increases many times over. Reserves become the main tool of the central bank to maintain financial market stability. However, the further dynamics of international reserves and the situation on the financial markets in Ukraine will depend not only on the state of the Ukrainian economy and finances, but to a greater extent on the level of international assistance from partner countries, cooperation with international financial institutions and, in particular, the continuation of the EFF program with the International Monetary Fund and further effective cooperation with external private lenders.

Thus, the main risks of deteriorating economic growth and accelerating inflation remain the intensification and longer duration of the war, further damage to industrial and energy facilities and critical infrastructure, and a possible gap between budget needs and the level of non-monetary financing of the budget. Macroeconomic risks also include a labor shortage in the labor market, which may result from the intensification of the war and increased emigration. Another significant risk is the lack of international assistance and its insufficient regularity, which is due to political processes in Ukraine’s partner countries. At the same time, there is a possibility of a number of relatively positive scenarios related to improved export opportunities, accelerated European integration of Ukraine and faster recovery of energy potential.

Undoubtedly, an important contribution to reducing risk impacts and strengthening the optimistic rather than pessimistic mood of the population would be to deepen communications about the current course of events and future plans that would involve not only the NBU. A demonstration of joint and coordinated work and joint adherence to the principle of “say what you mean and do what you say” would help to significantly neutralize the anxiety of both businesses and the public, thus having a positive impact on the economy.

Read this article in Ukrainian and russian.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google