Do banks fulfill their main function?

In the traditional sense, a financial intermediary is a market entity: commercial bank, investment bank, mutual fund, acting as a link between two parties to a financial or investment transaction, helping them achieve their goals. Financial intermediaries move funds from savers to potential investors with capital needs and are a key driver of economic growth. In fact, financial intermediation helps to create efficient markets and reduce the costs of doing business.

Unfortunately, financial intermediation remains underdeveloped in the economy of Ukraine, which slows down the process of transforming existing savings into investments. The share of bank loans in the structure of sources of financing investments and working capital of Ukrainian enterprises is less than 3%, the level of loans that are actively used does not exceed 10% of the Gross Domestic Product (GDP).

Over the past ten years, Ukrainian banks have turned from typical market structures into recipients of state funds.

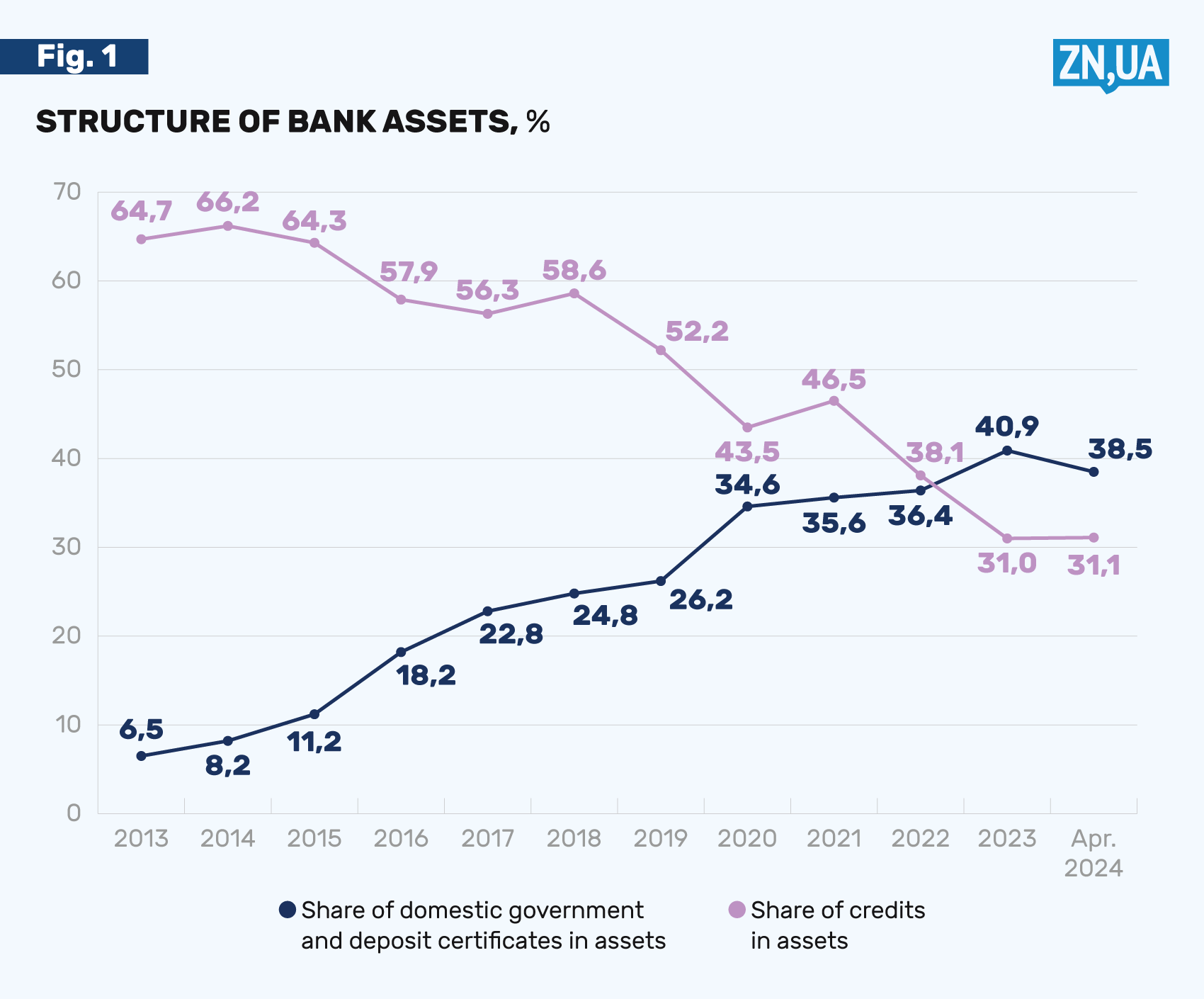

In 2013, the share of loans in the structure of bank assets exceeded 60%, and in 2024 it decreased to 30%. Instead, the share of banks' investments in state financial instruments (bonds of domestic state loans of Ukraine (BDSLU) and the National Bank of Ukraine (NBU) certificates of deposit) increased from 6.5% of total assets in 2013 to about 40% in 2024 (see Fig. 1).

The peak of the deformations in the work of the banking system were the years of the full-scale invasion of Russia. In 2023, a historic change took place in the structure of the assets of the banking system – for the first time since independence, the share of loans fell below the share of state financial instruments.

It should be noted that currently the banking system is one of the most state-subsidized areas of the national economy. And it is the state support in its various forms (bonds of domestic state loans of Ukraine (BDSLU), certificates of deposit, soft loans) that ensures the record stability, liquidity and profitability of the banking system, which the National Bank of Ukraine (NBU) likes to be proud of. The annual pre-tax profit of banks in 2023 reached over UAH 160 billion, and the Ministry of Finance of Ukraine was even forced to introduce a special tax on excess profits of banks at the rate of 50%.

Deformations in the structure of assets occur primarily as a result of inadequately high profitability of banks' investments in government bonds and deposit certificates of the National Bank of Ukraine (NBU). Today, the interest rate on three-month deposit certificates of the National Bank of Ukraine (NBU) is 16.5% per annum, which is five times higher than the annual rate of inflation.

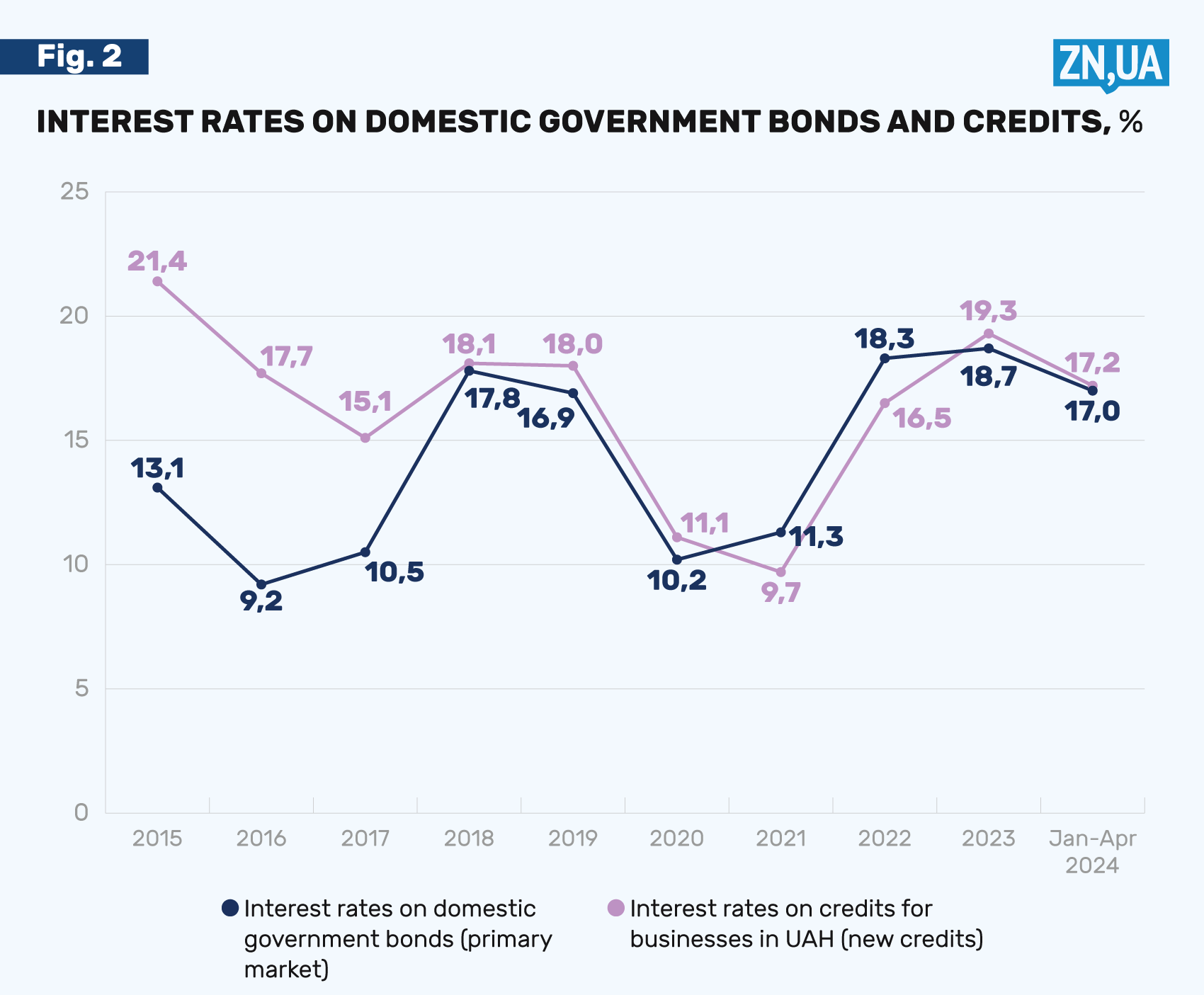

Since 2018, the average interest rate of new placements of bonds of domestic state loans of Ukraine (BDSLU) has almost coincided with the average rate of hryvnia business loans, and in some periods even exceeded it (see Fig. 2).

The formation of banks' profits occurs when the level of their financial intermediation decreases. Already during the war years, the level of lending by banks decreased from 15% of the Gross Domestic Product (GDP) to 10% of GDP for working loans.

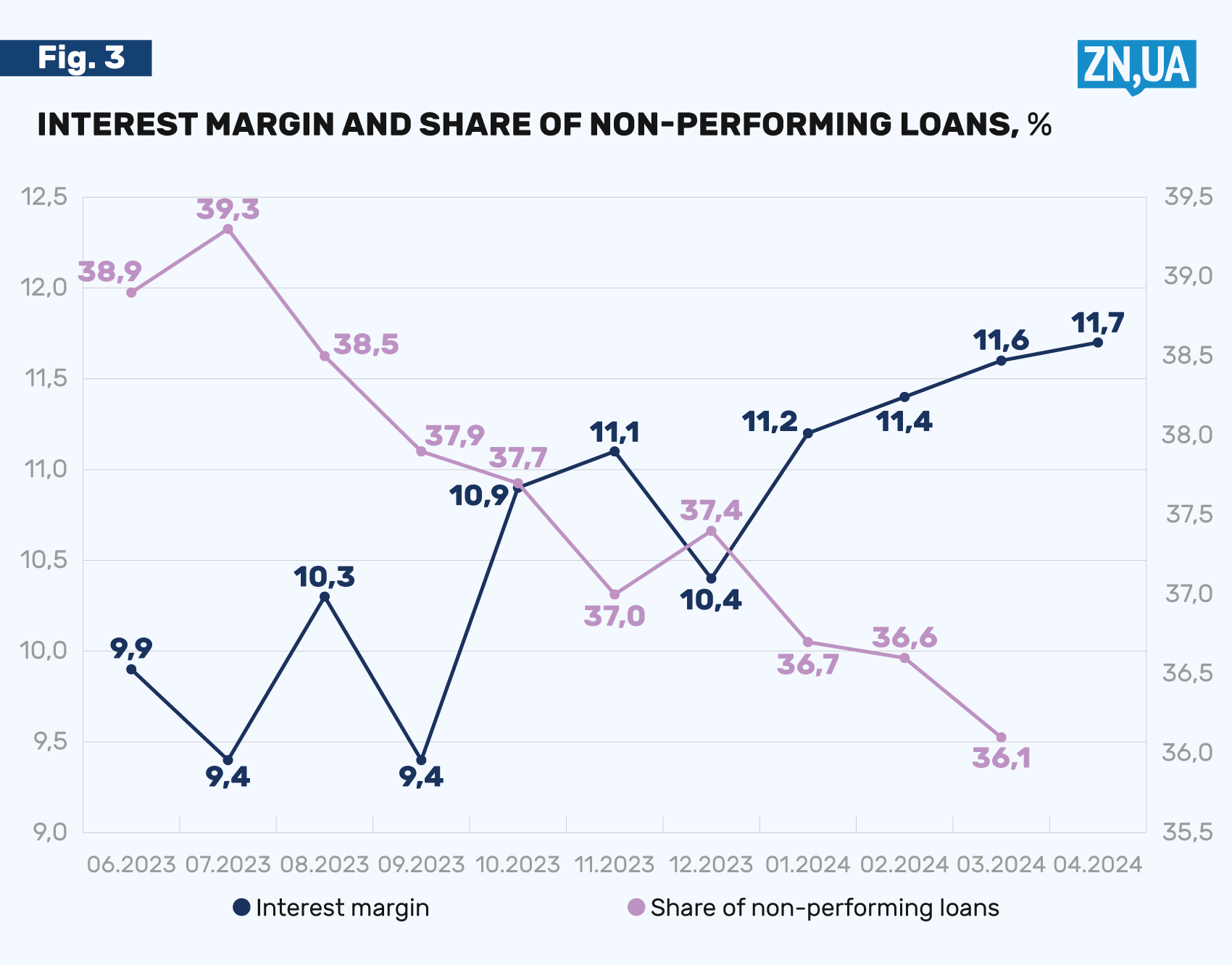

At the same time, the banks' interest margin between the rates for new loans and new deposits reaches gigantic proportions – 11.7 percentage points in April 2024. This is four times higher than inflation.

The interest margin of Ukrainian banks remains not only record high, it also continues to expand, despite the illogical decrease in the share of problem loans in bank portfolios (see Fig. 3).

In conditions of high interest margins, there is a double transfer of resources from the economy to the benefit of banks – owners of savings do not receive interest on deposits, and borrowers and investors pay inflated interest payments on bank loans.

Such a paradoxical situation was the result of large-scale state subsidization of banks and the banks' abuse of their market power. The presence of structural imbalances within the banking system prevents it from functioning as a healthy institution of financial intermediation.

The dominant component of bank profitability is formed by risk-free instruments for placement of liquid funds in the central bank, the interest rates of which are determined by directive, and not in accordance with market conditions. In 2023, the National Bank of Ukraine (NBU) spent UAH 91 billion, and in 2022 – UAH 41 billion to pay interest to banks on deposit certificates.

The source for the payment of these funds is the current interest income of the National Bank of Ukraine (NBU), the main part of which is the government's interest on the bonds of the domestic state loans of Ukraine (BDSLU), which amounts to (121 billion UAH as of 2023). Thus, large-scale payments in favor of banks were financed with the funds of the state budget of Ukraine (that is, with the funds of taxpayers and external donors).

The National Bank of Ukraine (NBU) claims that the extremely high discount rate and significant payments of interest income to banks on deposit certificates are the price that society must pay for maintaining price and currency stability.

However, this statement is not supported by either common sense or actual statistics.

It is unclear what positive consequences the central bank's interest rate policy, which ignores the critical condition and profitability of the real sector, and instead relies on artificial payments of the state on certificates of deposit, can lead to.

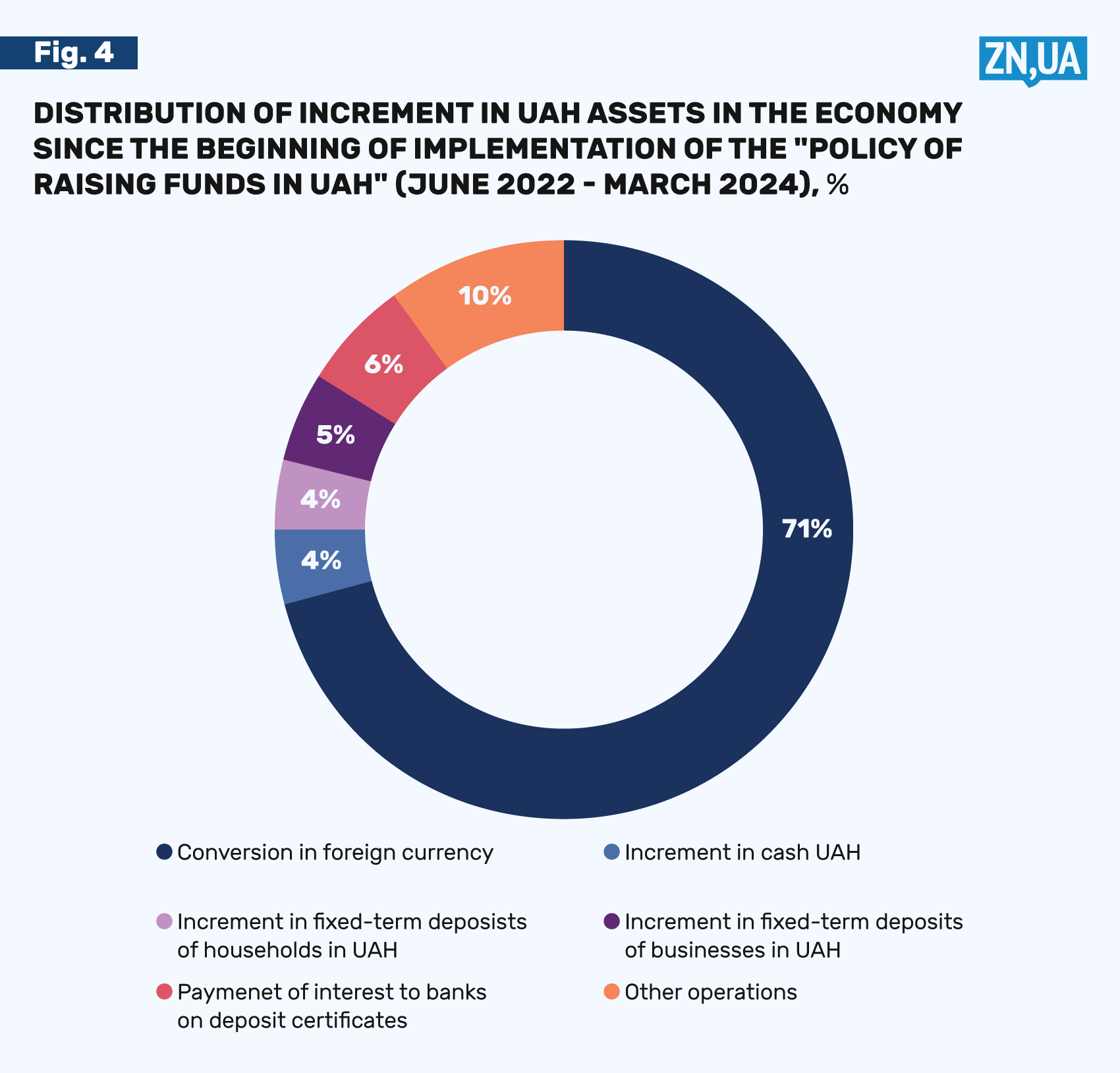

From the beginning of the implementation of the "policy of attracting hryvnia assets" (from June 2022) and until March 2024, UAH 2.6 trillion came into the banking system, mainly as a result of financing the fiscal deficit at the expense of international aid funds.

However, during the same period, banks attracted only UAH 230 billion of time hryvnia deposits from businesses and households (net increase). At the same time, only 107 billion hryvnias (less than 5%) settled in the deposits of the population. Economic entities (businesses and individuals) converted the majority of the new hryvnia liquidity into foreign currency – 71% of hryvnia funds, or UAH 1.8 trillion. Currently, most of the funds converted into foreign currency are in the form of cash currency outside banks, which has increased by 27 billion US dollars since the implementation of the "policy of attracting hryvnia assets".

The effects of the policy of "attracting hryvnia assets" (+ UAH 107 billion) were absolutely insignificant in terms of scale compared to both the volume of hryvnia monetary financing (2.6 trillion UAH from June 2022 to March 2024) and the structural deficit of the balance of payments (60.3 billion dollars from June 2022 to March 2024) (see Fig. 4).

That is, macroeconomic stability was ensured by factors independent of the monetary policy of the National Bank of Ukraine (NBU), namely, currency interventions by the National Bank of Ukraine (which amounted to 50.4 billion dollars for the corresponding period) and a drop in general demand (by 25% compared to the pre-war period).

The National Bank of Ukraine (NBU) even paid interest to banks on certificates of deposit more than these banks attracted funds from the population in "attractive hryvnia assets".

The multifold excess of the growth of currency assets in the economy over the growth of time hryvnia deposits became an objective indicator of the failure of the policy of attracting hryvnia assets. This state of affairs contrasts with the official statements of the monetary regulator. As a result of the described processes, the "policy of attracting hryvnia assets" could not have a significant impact on ensuring inflation and currency stability in the country.

All the given facts and trends signal that the efficiency of banks as financial intermediaries is extremely low, and the costs of implementing monetary policy are inadequately high.

Despite the fact that lending is the basic function of banks, the National Bank of Ukraine (NBU) has not received effective proposals for the development of market lending to the economy for ten years.

High interest rates in conditions of high war risks objectively and logically led to a reduction in the level of bank lending.

Moreover, official figures overshadow the fact that almost half of the bank's loan portfolio consists of soft loans supported by government programs. Government programs have already formed more than 40% of the banks' net loan portfolio.

High-yield certificates of deposit and government bonds have displaced loans to the real sector from the domestic debt market, making economic recovery more difficult. The narrowing of the credit loan market is particularly painful for Ukrainian business, as there are no other alternatives for attracting additional funds (such as the stock market, venture financing, etc.) in Ukraine.

The historical experience of countries experiencing military conflicts shows that in successful cases the real interest rate was lower than the growth rate of real Gross Domestic Product (GDP), which supported and stimulated the economy. In Ukraine, unfortunately, even the planning of prospective government policy is carried out with real interest rates that exceed the rates of projected real Gross Domestic Product (GDP) growth. ***

The policy of the National Bank of Ukraine (NBU) should be reoriented to real goals, namely the activation and improvement of the efficiency of financial intermediation, the development of monetary instruments supporting economic growth.

The demand for the national currency should be generated by increasing the number of national producers and the formation of localized production, and not by an artificial directive increase of the key interest rate of the National Bank of Ukraine (NBU), detached from the productivity of the real economy.

In the long term, the strength of the hryvnia and its exchange rate stability will be determined by the desire of economic entities to use it as a means of payment, as a means of lending and investing. And price and financial stability is always derived from the stability and competitiveness of the country's economic system.

Please select it with the mouse and press Ctrl+Enter or Submit a bug

Login with Google

Login with Google